|

|

|

June 11th, 2015 at 01:22 pm

I went to a stock options workshop at work. Now that the stock price has risen such that my vested options are worth a whopping $344K at fair market value (rising to $500K by year's end when more shares vest, assuming the price holds steady), I figured that it's finally time to learn how to deal with them.

I went into the workshop all happy and excited. I left decidedly less so, because I realized that I dun goofed pretty badly when it comes to tax planning.

My original plan was to buy out all of my ISOs with about $50K in cash in September, after the remaining shares vest, and hold them for long-term capital gains. I was also going to start selling off my NQs up to the Roth IRA AGI limit each year and move the money into more diversified investment vehicles.

Now that I've learned all about the AMT, I've realized that I can't do that.

I want to preface what's coming next by first saying that (my earlier Text is marriage penalty and Link is http://amberfocus.savingadvice.com/2015/03/26/the-marriage-penalty-is-brutal_196769/ marriage penalty post aside, which was more intended to be an analysis than actual griping) I almost NEVER complain about taxes. Furthermore, I HATE people -- especially rich people -- who complain about taxes. Yeah, I get that they're a pain, and it's not like I don't try to minimize/optimize my own tax bill (mostly because I try to minimize/optimize everything), but at the end of the day, taxes are the price you pay to live in a civilized society, as well as a "problem" that you only have if you've MADE MONEY. Making LESS money is still way better than making NO money.

But the phantom tax on ISO spreads? OMG, that's TOTAL BULLSHIT.

I know, I know, cry me a river -- but I am relatively certain that after I buy out my ISOs, I cannot afford the AMT that gets triggered on the $330K spread. I am FINE with paying taxes if I've actually made money, but I'd like to buy and hold in this case, which means that not only have I not made a dime, I've sunk in my own capital, and not even a nutjob like me has the kind of liquidity to afford the tax bill under the AMT. Not to mention the fact that triggering the AMT effectively negates all that is nice about ISOs relative to NQs.

I'm immensely frustrated right now, because I should've learned about all this way earlier. I should've been buying out my ISOs two years ago when the spread was much lower. I let the ball drop on this, and I'm kicking myself. As it stands, I'm gonna be spending the weekend plugging numbers into the AMT worksheet and seeing if there's any way to make this situation suck less.

I got all excited when I saw the stock price shoot up earlier this year. I thought that I could shave a few years off my FIRE date. I thought that if the market doesn't tank, maybe I could FIRE as early as 2017. Now I will probably have to throttle my ISO buyout to stay under the AMT threshold, and at the rate the stock (and my salary) is rising, I have no clue how long that's going to take.

I'm really trying to keep some perspective on all this. Yes, I got blindsided by the AMT with regards to exercising my ISOs, but even in the absolute worst-case scenario, in which I assume that half of my options are lost to taxes, my projections still have me reaching my FIRE goal of $1 million in three years, which is still two years ahead of how long it would take without any options at all.

I'll re-evaluate everything once I've worked out the AMT numbers. It is what it is and I'm still a lucky bastard no matter what. Once this is all sorted and I have a plan, I hope to not complain about taxes again for a long, long time.

Posted in

Planning,

Early Retirement

|

1 Comments »

May 21st, 2015 at 04:38 am

It tools weeks of wrangling, but multiple calls and e-mails to multiple insurance companies have paid off.

Last year, my homeowner's and auto insurance premiums were:

- home: $1031

- car #1: $1233 (comprehensive)

- car #2: $630 (liability)

- total: $2894

Now, after raising deductibles and lots of relentless haggling back and forth, I've gotten them reduced to:

- home: $676

- car #1: $620 (still comprehensive!)

- car #2: $267

- total: $1563

So I just saved $1,331 per year. Not bad at all. Between this and the $2715 savings in health insurance premiums when the SO and I both switched to high-deductible health plans, and this is a good year for insurance. Probably should have done this sooner, in retrospect, but from now on, I'm gonna keep a much closer eye on the insurance bill -- because jousting with insurance agents could be way worse.

Posted in

Quantitate!,

Groceries & Bills,

Home ownership

|

2 Comments »

May 18th, 2015 at 10:34 pm

Employer stock price went crazy and hit record highs today, and look at what happened in Mint --

I fully expect it to dip back below, but it sure was exciting to see assets hit seven figures for the first time. Maybe by this time next year, net worth will also be seven figures. One can dream.

Posted in

Early Retirement,

Investing

|

6 Comments »

April 13th, 2015 at 01:33 am

Posted in

Quantitate!

|

2 Comments »

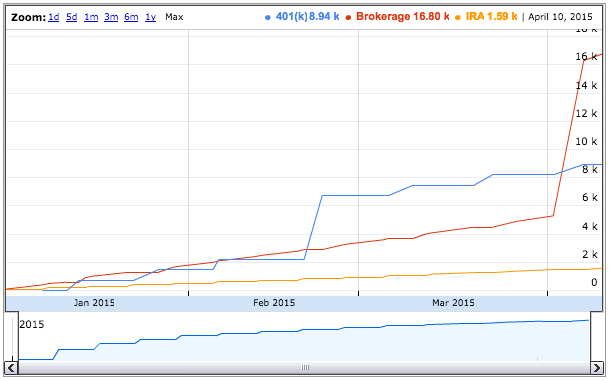

April 10th, 2015 at 08:51 am

Quick snapshot of the financial situation as of close of business 9-Apr-15:

Cash: $16,297.63

Home: $169,378 minus ($129,766.66) mortgage = $39,611.34 equity

Car: $13,900

Investments: $749,901.40

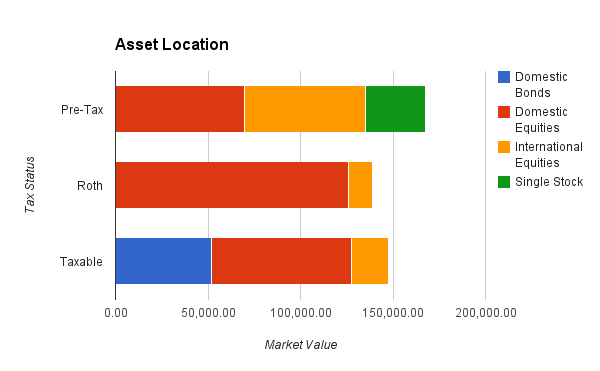

- 401(k): $113,746.98

- Roth IRA: $115,696.03

- Rollover IRA: $65,449.31

- Rollover IRA Brokerage: $9818.84

- HSA: $1132.78 (currently in cash; need $2500 minimum balance to invest)

- Taxable: $149,983.61

- Stock Options: $294,073.85 vested (out of $504,931.90 total)

Net Worth: $819,710.37

In recent weeks/months, I've made the following adjustments to my portfolio:

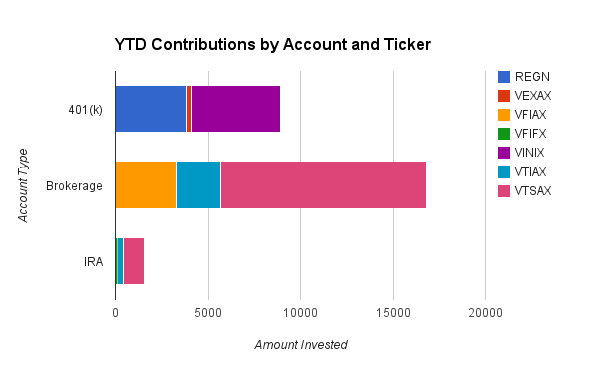

- Swapped 20% of my 401(k) from Vanguard Institutional Index (VINIX) to Vanguard Extended Market Index (VEXAX) to approximate the Vanguard Total Stock Market Index (VTSAX, which I can't get directly in my 401(k)), and balanced my future contributions to be an 80/20 split.

- Seeded $11K from money market into a taxable VTSAX holding, and will henceforth be using that instead of my S&P500 holding, which I'm retiring.

- Increased my taxable investments from $400/week to $500/week -- because I got a raise and bonus at the end of last year, and what else am I gonna do with it? :P

- Killed my (brand-new  ) traditional IRA. I apparently make too much money to take the deduction now. ) traditional IRA. I apparently make too much money to take the deduction now.

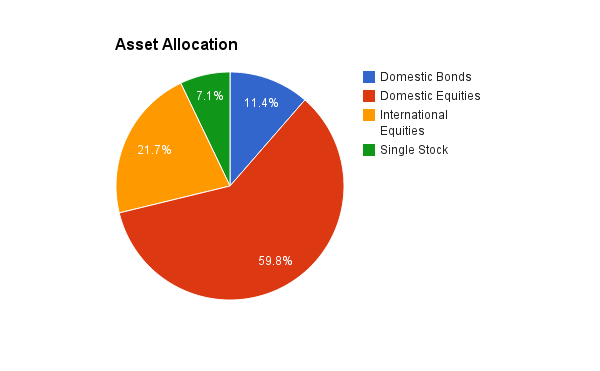

- I want my domestic to international equities ratio to be 2:1, but I'm at 2.76:1 right now, so I'm aggressively rebalancing my AA more towards international without triggering taxes. All of my Roth IRA and 80% of my taxable contributions are going towards Vanguard Total International (VTIAX). If this approach is taking too long (e.g. if by next quarter that ratio has barely shifted), I might buy/sell within my Roth space, or rebalance my 401(k) contributions.

I set a goal in Mint where I called reaching $1M in assets (excluding home/car equity and HSA) "FIRE", and the projected completion date is sometime in 2017 (April 27 at the moment, but it jumps around a lot). I love the fact that market appreciation is actually dwarfing my (fairly substantial) monthly contributions. Go Go Gadget Compound Interest!

Posted in

Quantitate!,

Early Retirement,

Investing

|

2 Comments »

March 27th, 2015 at 05:15 am

The SO and I have finished our tax returns for 2014. Just for funsies, we ran the numbers to see what our taxes would look like if we were to get married.

The results were NOT pretty. Essentially, my income would push him into a higher tax bracket that would nix his traditional IRA deduction, and his standard deduction would nix my itemized [mortgage interest] deduction... and we'd wind up paying an extra $2822 in federal taxes every year. It does not matter if we file jointly or separately -- the two are within six dollars of each other.

Even taking into account the savings of putting him on my employer health plan, marriage would still be a major net loss financially (and I'm not sure if spouses get their own HSA match). We don't have (nor do we ever want) kids, so that issue would does not apply, and other quantifiable benefits (like the spousal estate tax deduction) only apply if one of us dies. And in the case of my untimely early demise, I'd much rather leave my assets (with the exception of the house) to my parents anyway, since they need and deserve it way more.

Social Security is another consideration, but that won't be relevant for a while. And you only need to be married for one year to get spousal benefits, so there's no rush unless someone is actually dying (and I suspect if we're still together three decades from now that we'll be married by then anyway).

So what would it take for the marriage penalty to go away? Paying off the house would get rid of the itemized mortgage interest deduction for me, and the SO could get enough salary increases to phase out of the traditional IRA range all by his lonesome. We might hit the Roth IRA phase-out range faster if married, but I think that possibility is a more remote one due to how high that threshold is.

Joint high(er) incomes don't scale favorably regardless, but if I quit my job (due to achieving FIRE) and my earned income drops, then marriage could turn beneficial if we live off his income alone... but we'd have to run the numbers if I want to employ tax strategies like Roth conversion ladders. If we both FIRE on combined assets, then income would be too low trigger the penalty.

But in the current situation, I can only come to the conclusion that it makes NO sense to get married. I really want to at the very least break even. I realize that this is horribly unromantic, but this is just the way my mind works. I'm relentlessly rational, and the SO is similar, so we fit.

The next time my father nags me about not being married, maybe I'll just ask him to pay me three grand a year. That'll probably shut him up!

Posted in

Quantitate!

|

2 Comments »

March 25th, 2015 at 04:25 am

I've been taking steps in recent months to get my health care finances in order. During open enrollment at the end of last year, I switched to a high-deductible, HSA-eligible insurance plan, which dropped my annual premiums from $1690 down to $1144. Add in the $1000 HSA match that my employer kicks in, and I'm effectively paying only $144 per year for my health insurance. Even accounting for the new, higher $1500 deductible, I still come out on top.

And the out-of-pocket max of $3000 is definitely affordable in case I blow through the deductible due to a catastrophic circumstance.

Plus, I get a shiny new tax-advantaged investment vehicle to play with, which can be used to pay Medicare premiums or even function as a 401(k) when the time comes. Awesome. So I'm all set for the near-term.

Health insurance coverage and costs in early retirement might be more tricky -- or so I thought. One possibility is to go on the SO's employer plan -- that is, if he decides to continue working, and we actually get married. Currently, that would cost $1344 per year after adjusting for the $500 HSA match. Okay, so not nearly as good as my current employer plan, but is certainly tolerable.

But what if going on his plan is not an option? I certainly don't want him to keep working a job just for the health insurance if he doesn't want to!

We live in CT, so I went on our state health exchange to do research. I put in my expected FIRE income (which I guestimated at $10,000 if solo)... and kept getting bumped to the login page because, "Based on the income information you entered your household may be eligible for HUSKY D/Low Income Medicaid."

Erm... huh? I was so, so confused. I was expecting to look at subsidized private plans, not Medicaid. I mean, we may be freaks of nature, but we're certainly not poor, not if we're FIRE'd. Surely this can't be right?

But, as it turns out, with expanded CT Medicaid under the ACA, the Text is annual income limit and Link is http://www.huskyhealth.com/hh/lib/hh/pdf/HUSKYAnnualIncomeChart.pdf annual income limit for a single-person household is $16,243, and for a two-person household, it's $21,984. There are Text is no asset tests and Link is http://www.ct.gov/hh/cwp/view.asp?a=3573&q=421548 no asset tests for eligibility. No matter how you slice it, whether solo or married, we are going to come in under these limits post-FIRE, especially since these figures are for MAGI (modified adjusted gross income), and thus easy to manipulate using deductions and Roth distributions.

I Text is looked further and Link is http://www.favor-ct.org/CT_Medical_Home_Initiative/HUSKYManualFeb2014.pdf looked further into CT's implementation of the ACA, and Medicaid in particular. Apparently, ACA subsidies operate along a linear income scale. Above 400% FPL, there are no subsidies. Between 250% and 400% of FPL, one tier of subsidy kicks in (tax credits). Between 138% and 250% of FPL, a second tier of subsidy kicks in (cost-sharing).

Below 138% FPL, you are supposedly considered too poor to afford health insurance, and the subsidy is essentially 100%. And that means getting covered by Medicaid, where the government pays for all your health care costs.

There is no way to change what tier of subsidy you qualify for because it is predetermined by income. Furthermore, the subsidy is all-or-nothing -- you either take what's offered, or you turn down all subsidies. In my case, the choice is to either go on Medicaid, or pay full price for a private health plan. I don't have the option of getting a partially subsidized private plan.

And the cheapest private plan on the state exchange costs $2400 per year for a $6000 deductible, and goes quickly downhill from there. Yuck. And ouch?

I am honestly feeling seriously conflicted right now. On the one hand... it looks like health insurance will literally be completely free in FIRE (I actually spent quite a while trying to google "Medicaid premiums" before I finally realized how the program worked and that premiums don't exist). This is amazing and totally unexpected, since I've just been assuming that health insurance was going to be a major unknown expense in my projections. CT Medicaid Text is even covers dental and Link is https://www.ctdhp.com/default.asp even covers dental!

On the other hand... I feel so guilty (not to mention shocked) about potentially going on Medicaid. It is just strange to be mooching off a program intended for the socioeconomically disadvantaged. I mean, I am both willing and capable of paying a reasonable amount for health insurance. It's just that it genuinely looks like the program is working exactly as intended, and full price of a private plan is... kind of outrageous. How do you expect a rational decision-maker to turn down free given the alternative (or lack thereof)?

What does make me feel slightly better is the knowledge that on Medicaid, I would only cost the government money if I incur health care costs -- compared with an otherwise constant stream of private insurance premium subsidies. So the government might actually come out ahead, considering that I never go to the doctor (last time I went was in... 2007?) -- at least while I'm still young and healthy.

I think I'd budget $3K per year for health insurance anyway, just in case, but Medicaid being the preferred route is going to take some getting used to.

Posted in

Planning,

Early Retirement

|

5 Comments »

November 2nd, 2014 at 07:11 am

I have made the executive decision to no longer use a Target Retirement fund to manage my retirement asset allocation. That's right, the training wheels are finally coming off. It's time to learn to balance my investments on my own!

I have decided to make this change for a few reasons. The first is that the Vanguard Target Retirement funds charge fees based on the investor share class, and due to my portfolio size, I will save hundreds of dollars per year by moving over to the equivalent admiral share class. That's a good enough reason as any to make the switch, even if I wanted to keep the Target Retirement fund's pre-determined asset allocation. For a few hundred extra bucks per year, I am willing to deal with the so-called "inconvenience" of having to manually rebalance my investments.

Another reason to leave the Target Retirement fund is that I want the flexibility to change my asset allocation. Right now, the 2050 fund allocates 10% to bonds. I do hold bonds, but I'd rather hold them in my taxable accounts, and save the tax-advantaged space for equities with higher growth potential.

As an aside, I've heard the argument for holding less tax-efficient funds such as bonds and dividend-yielding stocks in the tax-advantaged space. My gut feeling, however, is that protecting equity growth and capital gains (especially in the Roth space, which not only grows but is also distributed tax-free) beats out protecting bond interest and dividends (which are designed to be lower), although I am totally willing to be convinced otherwise using math. Right now, though, I'm also using bond holdings specifically as a short- and intermediate-term savings vehicle, so I want them to be easily accessible in a non-retirement account.

I also realized that I am likely going to retire sooner than 2050 and may need to deviate from their glide path anyway, so I might as well cut the cord now.

As for how I'm handling the asset allocation... I have decided to hold a 70/30 split of Vanguard's Total Stock Market Index Fund and their Total International Stock Market Index Fund. This mirrors the Target Retirement 2050's exact ratio of these same two funds (at 63% and 27%) but without the bonds. In reality, this is slightly complicated by the fact that my active 401(k) is held in a separate account with different fund choices, but I'll get as close to this breakdown as I can. The larger goal is to force myself to start actively managing and rebalancing my asset allocation.

Posted in

Planning,

Early Retirement,

Investing

|

1 Comments »

October 5th, 2014 at 08:40 am

Yesterday, I did something I haven't done in years.

I went to the salon!

Back in January, my hair was getting extremely long and my co-worker offered to cut it for me. She seemed very confident (and had been asking to do it for months), so I agreed, but it did not take me long to realize that she bit off way more than she could chew. My hair is very thick, full, and slippery, and she was really struggling to cut through it. As tortuously long minutes ticked by and she continued to saw and hack and hem and haw, my distress level was starting to rise precipitously.

Finally, I had to put an end to it. I had started off with waist-length hair, and by the time I made her stop, my hair was down to chin-length, and could barely be tied back into a tiny, pathetic stub of a ponytail. The left side was visibly longer than the right, and the back was all sorts of different lengths. It looked, to put it bluntly, utterly ridiculous. I was completely traumatized by the experience.

But in the interest of good workplace relations, I had to smile and nod and pretend that I loved my new haircut -- as well as endure the painfully polite "compliments" from all my other friends and co-workers. There was nothing that I wanted to do more than to run to a salon and get everything fixed (in a wild moment of panic, I even considered hair extensions), but if I'd went out and got it redone immediately, the charade would have been up.

So I gritted my teeth, ironed my resolve, and spent the next nine months growing my hair back out. It has been a miserable, embarrassing, and painstakingly long wait, but the time has finally come that my hair is long enough to handle a trim without an immediately noticeable loss of length.

I found a coupon for a $9 haircut at a local salon, and went. I was extremely nervous after what I'd been through, but the stylist made me feel so comfortable, and he did exactly what I wanted, which was to even out everything while taking as little off as possible. The difference is subtle but immeasurable -- the comment from the SO was, "You actually look like you have a proper haircut now."

Lesson learned. Some tasks should best be left to the professionals. I don't think the trauma of the past nine months was worth a free haircut. I have never been so relieved to hand over money in a very long while. The guy certainly earned it. That $15 (I gave a $6 tip) was so worth my peace of mind... and my dignity. Whew.

Posted in

Expense Log,

A Day in the Life

|

3 Comments »

October 2nd, 2014 at 12:12 pm

Up until now, I've been using Roth IRAs exclusively. I just followed the extremely typical advice for young people to use a Roth, because it's better to pay taxes when one is younger, making less income, and thus in a lower tax bracket.

I also thought that the math worked out better, at least if one assumes a constant tax bracket. In a Roth, you pay your taxes up front, but everything after that grows and is withdrawn tax-free. It's a very simple FV calculation. In a traditional IRA, the same contribution amount goes in and grows tax-free, so you wind up with the same FV as the Roth, but the withdrawal is taxed.

This seems like a bad deal until you remember that you get to keep the taxes that you would've lost with the Roth. If you also invested the amount that you would've paid in taxes, and let that grow over time, it essentially makes up for the withdrawal taxes on the IRA itself, at least if the tax rate is the same. However, that investment with the saved taxes is outside of the IRA, so it is not tax-advantaged, so you actually wind up with less FV than if you'd just gone Roth to begin with.

So I managed to think through all of that, but for some reason, I never questioned the implicit assumption that my tax bracket in retirement would be the same as now (or higher). I guess I wanted to make sure that I "could" withdraw as much as I wanted in retirement, so I didn't see the harm in accepting that I'd have a high income in retirement.

Now that I'm properly thinking through my current income and expenses, it has become abundantly clear that this assumption is false. My savings rate is in excess of 50%, so I am spending nowhere near my current level of income, and my expenses are expected to drop even further once the mortgage is paid off. There is ZERO need for me to replace my current income, so I will be in a LOWER tax bracket in retirement -- and that's a good thing, because it makes FIRE that much easier to achieve.

So it seems like Roth has been the wrong way to go all along. I should've been using a traditional IRA and taking the tax break right now. Oh well.

I've gone and made myself a traditional IRA in Vanguard, and I'm swapping over to it. I may even inquire about recharacterizing this year's contributions. This just goes to show that always assuming a worst-case scenario can cost ya.

(I also have another reason why I'm interested in switching to traditional, and that has to do with the Roth Conversion Ladder, which I'm learning about right now. Maybe I'll write it about it later, after I've got it worked out in my head.)

Posted in

Quantitate!,

Planning,

Early Retirement

|

2 Comments »

October 1st, 2014 at 11:36 am

Out of laziness and expedience, I handle almost all of my money management passively. All bills that stay constant month-to-month are on auto-pay, and investments are either on payroll deduction or auto-drafted on a weekly basis. To avoid accidental overdrafts, I keep my checking balance very high, and my cashflows are generally positive. As a result of this setup, I can go for a fairly long time without looking at my bank accounts.

A side effect of this passive approach is that a lot of cash accumulates in my checking account when I'm not paying attention. Every once in a while, I'll pop in and transfer a few grand out into savings and/or bump up my investments, but those actions weren't aggressive enough to prevent my cash holdings from topping $75K in recent months.

I know that $75K is too much to hold in cash. Following the standard advice of keeping 6 to 12 months of Text is expenses and Link is http://amberfocus.savingadvice.com/2014/09/12/comprehensive-spending-review_152268/ expenses in liquid assets, I should only be holding around $15K (+/- $5K). After my car purchase in 2012, which was my biggest anticipated expense, there's been no need to hold additional cash on hand.

So if I'm committed to holding no more than $15K in cash, where should I put the remaining $60K? The lowest hanging fruit by far was to pay off my student loans, so Text is I did that and Link is http://amberfocus.savingadvice.com/2014/09/15/sayonara-sallie-mae_153177/ I did that. Boom, that took care of $7K, and Sallie Mae is out of my hair for good. But that still leaves $50K or so that still needs a good home.

One obvious option is to sink it all into equities, and that is a reasonable suggestion, given my long timelines and high(ish) risk tolerance. But I'm hesitating on taking this course of action for a few reasons. The first is that I don't feel like I'm underexposed to stocks. In my (half-hearted) attempts to drain my checking balance, I've already increased my automatic investments to $400 per week, to the point where my cashflow is now pushed into the negative. (I should be fine after my year-end bonus/raise, though.) Combine that with my maxed out 401(k) and IRA contributions, and I'm sitting at $43,800 worth of stock purchases per year. That's half of my base (gross!) salary, so I can hardly be accused of not investing enough.

A slightly more tangible objection to the lump sum stock investment idea is that I am in the process of researching and planning what to do with all of my stock options. I'm looking into this because I've already vested into quite a large number of shares, but action is not necessarily imminent because I've still got a few more years to go in terms of vesting into the rest. However, if I'm interested in a buy-and-hold cash exercise, I will need a considerable amount of cash up front (tens of thousands, easily). I'm concerned that if I tie up all my money in equities right now, I may not be able to pull it out in the next few years if I wanted to do a cash exercise. But the time horizon is still long enough that it seems a shame to not invest at all.

So I've decided to compromise. I bought some bonds instead! Specifically, I got the Text is Vanguard Intermediate-Term Investment-Grade Fund Admiral Shares and Link is https://personal.vanguard.com/us/funds/snapshot?FundId=0571&FundIntExt=INT Vanguard Intermediate-Term Investment-Grade Fund Admiral Sha..., which (coincidentally!) has a minimum balance of $50K. This fund holds, according to its description, "diversified exposure to medium- and high-quality investment-grade bonds with an average maturity of five to ten years" by investing in "corporate bonds, pooled consumer loans, and U.S. government bonds within that maturity range". That seems consistent with both my time scale and risk tolerance. I do understand how bond prices work in conjunction with today's insanely low interest rates, but bonds are designed to provide steady income and returns, and it's got to beat the return on my savings account.

In conclusion: I've successfully ditched my cash! I am not buying more stock, but I am still investing. I suspect I'm be done with direct bond purchases for the time being, and may even allocate any returns back towards equities, but at least I don't have $50K burning a hole in my pocket any more.

Bon(d) voyage!

Posted in

Planning,

Investing

|

4 Comments »

September 27th, 2014 at 09:28 pm

I realize that pensions are rare like unicorns these days, but I actually have a small one under a previous employer. It's not worth much because I only worked there for three and a half years before being laid off, but the pension is supposed to pay out $261.88 per month starting in 2049 (when I turn 65).

They are now offering what I presume is a buyout. I can either:

1. Roll over a lump sum to an IRA or another employer's qualified plan ($6352.78).

2. Take a lump sum cash distribution ($5082.22).

3. Start monthly payments now ($24.71).

4. Retain the original pension benefit.

Should I take it? To figure out if this is a good deal, I calculated the present value of this future annuity.

Step one: Calculate the PV of the annuity at age 65. I'm arbitrarily using an interest rate of 6%, and a life expectancy of 100 (so 35 years).

PV(0.06/12,12*35,261.88) = $45,928.57

Step two: Discount that to today's dollars using the same rate.

PV(0.06,2049-2014,0,45928.57) = $5975.55

So it looks like the lump sum payment is a reasonable offer. I'm also assuming an extremely long life expectancy, which would bias the value upward. I'm not sure what rate I should use, but 6% is a figure I can hope to beat by investing on my own. I've tried plugging in different interest rates, but that causes the PV to fluctuate wildly.

I am really tempted to take it. If I roll it into an IRA now, I know I'll have control of and access to it before age 65, which is particularly helpful if I'm planning ER. I also avoid the risk of the company underfunding, raiding, or otherwise reneging on their obligation (I'm looking at you, Hostess) anytime in the next 35 years. I have so far been completely ignoring my pension in retirement planning, so this would allow me to take it into account.

I have until month's end to decide. Hmm.

Posted in

Quantitate!,

Planning,

Early Retirement,

Investing

|

9 Comments »

September 26th, 2014 at 09:26 am

I was discussing Text is this article and Link is http://www.entrepreneur.com/article/234454 this article with someone online the other day, and when I mentioned that the SO and I actually did reach millionaire status by age ~30 via saving rather than focusing on income, I received what I initially thought was an odd response.

"But you don't have a million dollars in liquid cash", he said. "Stocks can go down as well as up!"

At first, I was really confused, because that comment was clearly meant as a dig, as if holding investments worth a million dollars is somehow not as legitimate as having a million dollars in cash, simply because the market could go down, but who in their right minds would (unless one were running a corporation) hold that much in cash?

But then I started to unpack the implicit assumptions in his statement, and I came to a few realizations about his point-of-view.

His comment makes the assumption (like many other people, I'm sure), that being "rich" or "wealthy" is about having a lot of money. But that is not the right way to think about it. Conceptually, money is merely an abstract representation of value, and cash is just a single form of that value. The technical and more inclusive term for "stuff with value" is "assets", and that includes anything that has monetary worth, whether it's cold hard cash, a stock portfolio, physical property, or a business.

Most individuals who are wealthy hold their net worth primarily in assets, not in cash, and there's a reason for that -- cash is static in value. I have taken three finance classes, and every single one of them opened with TVM, or the time value of money, which is a fundamental concept in finance that the value of money does not stay constant; it changes over time according to an interest or a market rate. Thus, in order for money to hold its purchasing power, it needs to earn an interest rate that is at least equivalent to inflation. That usually means not holding assets as cash, which can only depreciate over time, but as investments, which can appreciate over time.

The second part of his comment, about market fluctuations, assumes that a down market means you've lost money. But those losses are purely on paper, and would not be realized until the assets were sold, which any prudent investor should refrain from doing (if they can help it). I didn't panic at all in 2008; that was actually the year I switched to a much higher-paying job, and started hitting the 401(k) as hard as I could. And I plan on calmly riding out any future market downturns, so I'm not too phased by unrealized short-term capital losses.

Furthermore, there is another fundamental theory in finance called the Text is Capital Asset Pricing Model, or CAPM and Link is http://www.investopedia.com/articles/06/capm.asp Capital Asset Pricing Model, or CAPM. The basic take-home message of CAPM, as I understand it, is that risk and reward go hand-in-hand. (I don't claim to have a sophisticated understanding of finance theory, but not only was CAPM taught in finance class, it also Text is won the Nobel Prize in economics and Link is http://www.nobelprize.org/nobel_prizes/economic-sciences/laureates/1990/press.html won the Nobel Prize in economics, so I assume it's not completely full of shit.) I am chasing returns at this time, so I'm fine with taking on some risk. I am not going to fall for the trap of Text is loss aversion and Link is http://en.wikipedia.org/wiki/Loss_aversion loss aversion like he seems to be, especially when I don't invest anything that I'm going to need anyway.

It's fairly unfortunate when people hold onto these incorrect assumptions, and they don't have a more mature understanding of how finances work. I feel like I've barely scratched the surface of this vast and fascinating topic, but what little I do know already makes a huge difference in how I approach my finances.

And that knowledge is power.

Posted in

Musings

|

4 Comments »

September 23rd, 2014 at 02:09 pm

How much does one need to retire securely?

I've been trying to answer this age-old question ever since I learned how to spreadsheet. In fact, my Google Drive is littered with the desiccated remains of various retirement projection spreadsheets that I've attempted over the years, but could never figure out how to finish. Usually, it ends with me throwing up my hands and going, "It's a pointless crapshoot to try to guess 40 years into the future, but it's impossible to overshoot it at this juncture, so just maximize the sh*t out this, and you can figure out the details later."

That has been a pretty good approach up to now, but if I really want to FIRE it up in the next decade or so, I need to set actual goals and criteria for success.

I know that the standard guideline for having enough retirement savings is the 4% rule. So if your expenses total no more than 4% of your nest egg, then your nest egg can sustain you indefinitely, assuming a 7% rate of return with inflation at 3%.

And that's where I start getting twitchy. Can you really count on 7% returns in perpetuity? I know that's (more or less) the historical long-term stock market average, but there's no way to know for sure what future returns will look like. Plus, I would need to be sustained for many decades longer than a normal retiree, which makes projections even more difficult to make. I don't want to run out of money, especially given the fact that I can easily continue working and I don't have to take early retirement at all in the first place.

What I'm getting at is that I am very risk-averse and financially conservative. And I don't mean risk-averse in the sense of investing; on the contrary, I'm fairly risk-tolerant there because I know my timelines are flexible. I'm risk-averse in the sense that my mind always jumps to worst-case scenarios. I don't like being on the edge. My natural tendency is to save and save and save, because I don't know what could happen tomorrow and I might need that cushion. I could lose my job. (Actually, been there, done that. :P) Or come down with cancer. A tree (or a meteor) could fall on the house. The SO's Beetle could get creamed by a Mack truck. The possibilities for catastrophe are endless.

As a result of this rampant paranoia, I need to build in a large safety margin. I need to know that I can survive anything, and I'm not decreasing my financial resilience by giving up a fairly nice income. But I also want to be somewhat realistic and not let irrational fears and rampant goal inflation make FIRE unattainable, even though the honest truth is that I'd be terrified.

But I'm gonna force myself to come up with something just to get the ball rolling.

My current thought process is that I have two criteria that must be fulfilled before I would feel comfortable declaring FIRE -- a paid-off house, and two million in assets.

The paid-off house is pretty straightforward. As detailed in my Text is recent spending review and Link is http://amberfocus.savingadvice.com/2014/09/12/comprehensive-spending-review_152268/ recent spending review, the mortgage is by far our largest fixed expense, and knocking that out alone would drop our annual spending from $40K down to $25K, with another $5K being shaved off when I stop renting in and driving to/from NY. Furthermore, the mortgage is something that needs to be done sooner or later. We're already paying extra towards the mortgage every month, and we're on track to paying it off in about ten years.

As for the two million in assets... We already have $1M, which, according to a 4% withdrawal rate, could already (in theory, with proper allocations, etc.) support our current $40K in annual expenses. But as I've already said, I don't feel even remotely safe enough with a 4% SWR. With a two million dollar portfolio and ~$20K in expenses, that would be a 1% SWR, which I think is conservative enough. And even if something horrible were to happen to the SO, I should still be able to handle a 2% SWR on my half of the two million. And there's even wiggle room to increase spending if it really came to that.

So I think the preliminary goals for FIRE should be no mortgage and $2M. I would not be too surprised if I chicken out and raise/revise it later, but this seems reasonable for the time being. I'm already thinking that home equity and inaccessible retirement vehicles shouldn't be included in the $2M, but we'll cross that bridge when we come to it.

And I've also got some time before we reach the goal to work on emotional readiness and all that jazz.

Posted in

Musings,

Planning,

Early Retirement

|

3 Comments »

September 18th, 2014 at 01:11 pm

Convo from this morning, with the SO who also paid off his student loans earlier this year --

SO: I wanted to have a FUCK YEAH NO MORE STUDENT LOANS reward.

SO: But then I did the thing I always do when I attempt to reward myself.

SO: Go: "Do I really need to?"

SO: But maybe we can have a nice Fuck Student Loans dinner some day.

SO: Probably not.

Me: Why don't we have a nice Fuck Student Loans purchase of leeks, and make, I dunno… pho or something.

SO: Snicker.

SO: AWW YEAH.

SO: Sounds good.

(Pho is one of our favorite meals, but we shop sales 90% of the time and leeks are NEVER on sale.)

And for anyone who's keeping track, we did not get the celebratory walnuts last weekend (still balked at the price when not on sale, heh), but we did get a $2 bag (14-oz) of discontinued Skittles from Ocean State Job Lot, because apparently Skittles went gelatin-free in 2010, and I HAD NO IDEA. I haven't had Skittles since 2002 (when I went veg), so I was totes excited.

I love that we can appreciate the little, inexpensive things. They honestly make us way happier than typical consumerism.

Posted in

A Day in the Life

|

3 Comments »

September 15th, 2014 at 04:16 pm

I just paid off the remaining balance on my student loan. I just wanted it to be over and done with, and I had the cash sitting in my checking account (earning zero interest) anyway.

I used their loan payoff calculator, which insisted that it took two days for an electronic transfer to go through. It didn't, so I wound up overpaying by 67 cents.

They better give me my extra 67 cents back...

Posted in

Uncategorized

|

4 Comments »

September 15th, 2014 at 04:01 pm

Face punch time! Car maintenance this weekend with the final damage at $232.40 for oil change, air filter replacement, tire rotation, and re-balance. Looking at the itemization, a large chunk of that was labor.

Well, at least nothing else was off, and I'm done with this nonsense for another 9 months.

Posted in

Expense Log

|

1 Comments »

September 12th, 2014 at 12:45 pm

I recently compiled a somewhat exhaustive record our household's monthly and annualized expenditures, I thought I'd share it on the blog.

Housing - $20,739

The mortgage, at $1377/mo or $16,519/yr, is the biggest housing expense, and it includes $2600 property tax and $1031 in homeowner's insurance. I work out-of-state, two hours away from home, so I also rent a room near work where I stay during the work week, which comes out to $310/mo or $3720/yr. I also budget in $500 for various DIY projects such as deck staining and weed whackers.

This is by far the largest part of our annual expenditures, and I’ll talk more about it at the end.

Utilities - $1760

Electricity usage per month is around 320 kWh, which comes out to $60/mo. Water usage is typically 100 cubic feet, or $20/mo. Internet (cable modem) is $30/mo. We don't have (nor do we want) cable TV. Trash and recycling pickup is $20/mo. Cellphones are currently free, because the SO gets reimbursed by his employer and I'm mooching off my parents' plan. Heating oil is spiky and my records aren't great because the SO orders the oil, but I'm guestimating it's about $200/yr.

I'm using long-term (two year) averages for the utility figures, so I think they're fairly accurate. Heating oil is the only exception, because that is highly dependent on the price of oil and the winter weather, but we already keep the thermostat in the low 50s so there’s not much more that can be done there anyway. The only area we might be able to reduce is trash pickup, because we don't generate enough trash to need weekly pickup, but my address is not allowed to use the dump, so I'm kind of stuck hiring a service. If there's no cost to cancelling and resubscribing, I might just sign up for a month of trash pickup a few times a year, but I'd have to look into that.

Automotive - $5413

Currently, we have two cars. Mine is 2 years old, the SO's is 14 years old, and both are paid off. Insurance is costing $1233/yr for comprehensive collision for my car, and $630/yr on liability for his. My maintenance costs are $120 for 2 oil changes per year, but the costs on the 14-year-old car are much higher; maybe $1200 or so? I haven’t really been tracking his car repair expenses, but I'm gonna try to start doing that now. As for gas, mine is around $1300. I have no idea what the SO spends on gas, because he rides in a carpool most of the time and he doesn't track his fill-ups as maniacally as I do, but since he does all the local driving to the grocery stores, I’m guestimating it at $600/yr.

In some ways, cars are a discretionary cost, but we're in a small town, and a car is our primary means of transportation. I have done the research on the public transport options in the area, and it is wildly inconvenient to go to the grocery store or the dentist's office by bus. We also travel regularly to see family out-of-state, and while it's possible to make the trip on public transportation, it was time-consuming and not fun at all. There is also the issue of potential emergencies, like rushing the cat to the vet. At the end of the day, we think it is worth it to spend the money for the convenience of having a car.

With that said, I would love to drop down to a single car in the future. A used but not-too-crappy car would keep both amortized costs and insurance low. Aside from the work commute and grocery runs, we don't drive much anyway, so if I can ditch my commute, I don't think we'd still need two cars. That would save a few grand a year.

Medical - $4682

The SO and myself both get medical and dental insurance through our work. Our health premiums are $1690/yr (me) and $2513/yr (SO), and our dental is $156/yr, and $224/yr. I also threw his $100 annual deductible into the budget, but I haven't been to a doctor in 7 yr (I know! I’m terrible! I better not have cancer). It's kind of sad, how different our health plans are, because even if the SO switched to a high-deductible HSA-eligible plan, his annual premium would still be $1844, which is higher than my normal plan, but it's actually a fair price for insurance.

I half-joke that we should get married just so I can put him on my health plan and save almost $1000 a year. Even taking into account the amount we'd spend on a wedding, we'd break even after a year or two, heh.

Consumables - $5100

This category encompasses all the regular, discretionary but non-emergency spending, including food and entertainment. The figure that drove the last financial advisor crazy was the $160/mo ($1920/yr) I put down for groceries. Yes, that's what we spend, and no, we don't live on ramen (unless it’s homemade, delicious ginger tempeh soup with ramen and bok choy). I don't really dine out either, because unless I'm in a college town or a specialized restaurant, the vegetarian options tend to be either nonexistent or wholly uninspired. The SO does spend $40/wk going out to lunch, but that is how he pays for his carpool, so it should probably count towards the transportation budget. Between these two items, that’s $4000/yr.

Aside from food, the rest of the discretionary budget covers entertainment (generally either Netflix or various video games), pets, and odds 'n ends such as gifts and other miscellaneous purchases. The most costly indulgence is the Broadway tickets we get once a year, but aside from that one night out, I prefer staycations to vacations. All of those total no more than $1000/yr.

Total - $37,695

One-Time Large Expenditures - ???

We do encounter occasional, isolated, large expenditures which I’m not including in the regular budget, but we do have to take into account. Last year, I traveled to California for a wedding, and we had veterinary emergency, all of which cost more than $3000. This year, housing maintenance is shaping up to be the big unanticipated expense.

ANALYSIS

So housing takes up the bulk of annual expenditures. Paying off the mortgage alone would drop expenses down to $25K. If I'm no longer renting and driving out-of-state, that would chop off another $5K, and would drop annual expenditures down to $20K. Most of the other categories, such as utilities and medical/dental premiums, are fairly inelastic. We definitely need both cars right now, but maybe we won't in the future. There isn't much fat to trim in consumables, either.

At our current expense level, I would have to bring in $40K / 2 = $20K to maintain our lifestyle. After the mortgage is paid off, I'd only have to bring in $10K to $13K. Obviously this may change, but I am wracking my brain for what I might want to spend more on, and I'm honestly drawing a blank. I’ve never been big on consumerism, and the only areas where I enjoy spending money is food/cooking and pets. And the pets kind of prevent me from being able to have nice things anyway, because it's all just gonna get shredded by sharp (but adorable!) claws and teeth.

What's way more important to me than planning for possibly higher future spending is making sure that I can be fully independent without the SO -- because he might get run over by a truck tomorrow (yes, that is how my mind operates). That means being able to handle the doubling of all expenditures. This is absolutely essential to my peace of mind, and will likely result in a ton of overcompensation in retirement planning/projections, but I'm okay with that. At the end of the day, I'm the only one that I can truly count on.

Posted in

Quantitate!,

Expense Log,

Planning

|

3 Comments »

September 11th, 2014 at 02:04 am

Yesterday, I vested into some more of my employee stock options, the ones I got three years ago before the stock price shot up almost six fold. I logged onto Mint and checked my net worth -- it's jumped up to almost up to $600K.

Out of curiosity, I then asked the SO for the balances on his accounts, and added everything up, and… holy moly.

Together, we are now worth over one million dollars. We are officially millionaires. (WHAT!! Whoa.) It's a bit surreal. We are now, in actual fact, the millionaire(s?) next door.

And we shall celebrate this fact with walnuts.

Posted in

A Day in the Life,

Investing

|

7 Comments »

July 8th, 2014 at 10:47 pm

My workplace will occasionally bring in financial advisors to give seminars and one-on-one consultations. I've been to two of these sessions, meeting with three advisors total, the most recent of which was just this past week, and have come away frustrated at the lack of productivity every time.

I understand that it's a free service, the scope of their help is limited by time, and they're likely not expecting someone like me, but I think it goes beyond that.

The main crux of the issue is that we simply don't see eye-to-eye philosophically.

For this most recent meeting, I tried to go prepared. In the past, showing my various account balances just resulted in sputters of disbelief and a request to repeat my age, so I brought my complete Social Security earnings history. When I say that my spending is such that a withdrawal rate of $20K is sufficient to maintain my lifestyle, I get asked what kind of car I drive and what model phone I have, so I actually tallied up the entirety of my annual spending to demonstrate that I am not, in fact, grossly underestimating my expenses.

But it didn't work. I still got asked to repeat my age. I still got told soothingly that "circumstances change", that expenses rise over time, and that once I get used to a higher standard of living, it's difficult to go back. The advisor took one look at the grocery line on my budget and told me, pityingly, "Well, you don't look like you eat much".

That last comment just made me laugh, because it shows how deceiving appearances can be. Now, I am a tiny, tiny person, so I guess it might seem like I "don't eat much", but that's not the case at all. I actually love eating and cooking, and I even briefly attended culinary school and worked as a prep cook at a restaurant before my pharmaceutical career took off. Our pantry is stocked to the brim, we make all our food from scratch, and we eat like kings -- all on a fraction of the cost of average households.

But what's more, that comment also betrayed the tacit assumptions made by the advisor. I am tiny because I don't eat, and she feels sorry for me because she assumed that I'm purposefully depriving myself, and that I will let it go at some point. It's fairly galling to me, mostly because it really reminds me of the condescending comments I've gotten my entire life when I tell people that I don't want kids, and they're like, "Oh, you may say that NOW, but just wait and see..."

Um, no. I know what I want, it's not the same as what you want, please don't project yourself onto me while ignoring what I actually say, because it causes you to come to incorrect conclusions about me, which makes me quite grumpy.

The truth of the matter is, at our current level of spending, we have almost everything we could possibly want, and I frankly don't know what else to spend money on. I don't want a bigger house; I actually prefer it small and cozy. I don't want a fancy car -- I barely even want a car at all, although I accept that I need one at the present time. I don't want a smartphone, I'm perfectly fine with my six year old phone, and I don't even have texting or a data plan.

And as for food... When I can make gorgeous artisan bread for less than a dollar per loaf, why would I ever want to spend more? And even if I go hog-wild and stop subbing walnuts for pine nuts in my pesto recipe because pine nuts are too expensive, I still don't see my grocery bill increasing by that much, because at the end of the day, any raw ingredients, even pine nuts, simply don't add up to more than a few hundred dollars a year.

Perhaps the hardest fact for these financial advisors to wrap their heads around is that I really and truly do not find consumerism to be all that appealing. For me, frugality is not a form of masochistic self-deprivation; I genuinely find it much more satisfying to live a simple and efficient lifestyle. As a result of these dispositional differences, all of their advice and experience is predicated on a set of assumptions that do not apply to me.

I think this is a big part of why haven't felt comfortable and in sync with these financial advisors. (Hell, I think this is a big part of why I feel out of place in this world. :P)

There was a bit of good news that came out of this session, though. After I finally got her to stop fighting me on the validity of my numbers, she conceded that she does think I can early retire in ten years. Actually, she doesn't think I need more than five years, especially if I can line up a side hustle. Obviously, I won't just take her word for it, but at least this tells me that I'm not on a wild goose chase. This is a realistic and achievable goal.

I just have to work out all the details.

Posted in

Musings,

Planning,

A Day in the Life,

Early Retirement

|

4 Comments »

July 1st, 2014 at 07:27 pm

I adore watermelon -- it is one of my favorite fruits. I'm generally not a big fan of summer (too hot, and sweating is gross), but one thing I do look forward to is watermelon.

This week, one of the loss leaders at my local Stop 'n Shop was a whole watermelon for $3.99.

I picked through the bin, tapping and weighing each one, until I found a behemoth that clocked in at 20.62 lbs.

Afterwards, I ran the math -- $3.99 / 20.62 lb = $0.19 per lb

Hee! I am very pleased with myself.

Posted in

Quantitate!,

Groceries & Bills,

A Day in the Life

|

2 Comments »

June 26th, 2014 at 07:05 am

Back in the beginning of May, during a particularly heavy storm, water seeped into the basement of our raised ranch, and a small patch of carpet got wet.

I'm not home much at all (I work out of state so the only person at home during the week is the SO), and we don't spend much time downstairs in the basement, but as far as we're aware, this was the first time water had gotten into the house.

All right, it's confession time. I'm a few different things, but handy is not one of them. I grew up in city apartments with my nose buried in books, and I'm lucky if I can identify -- much less wield -- a screwdriver. The SO is also very mechanically/manually challenged. He is utterly flummoxed by wonton wrappers and never learned how to ride a bike.

Suffice it to say -- neither of us had any clue what to do. How big of a deal was this leak? Is it a sign of progressively bigger problems to come? Or was it a one-time fluke due to extraordinarily heavy rainfall? I wasn't there to see it happen, so I don't even have a sold conception of how much water there was, although the SO claimed he blotted through an entire roll of paper towels. (But have you also seen boys with paper towels? Do they ever use less than an entire roll on a spill?)

So we try to investigate what might be wrong. There might be a small crack in the foundation where the leak was, but maybe it's been there all along and is just superficial. The gutters weren't quite sloped right and were dripping a bit. The ground near the house has settled a bit, so some water is running/pooling against the side of the house.

Any or all of these could be plausible explanations for the water, but given our lack of expertise in these matters and the number of 'horror stories' one finds on the internet, I feel like I have the housing equivalent of medical students' disease.

First, the SO called some "dry basement" people. It turns out that they all want to tear up the floor of the basement, drill holes in the foundation, let all the water in to relieve the hydraulic pressure, and pump it out with a sump pump and generator -- all to the price tag of $3000 to $10,000. Um, WTF? No thanks, it was a bit of wet carpet, not a full on flood.

Then he called some gutter people, thinking that it's fairly low-hanging fruit, since the gutters shouldn't be dripping anyway, even if the drip is unlikely to be the sole cause of the water. Their offers ranged from a basic repair/tune-up to fancy patented proprietary systems.

Shortly after the initial leak, the SO dug a trench that re-routed most of the runoff around the house. It was kind of hideous looking, but it was definitely catching the water, and there hasn't been another leak since. He wasn't sure if the amateur trench would hold, so he called professional landscapers. Those proposals ranged from "Why are you wasting my time with something so minor? Call me back when you have a real problem to fix" to multi-thousand dollar projects.

If I'm being totally honest, I'm not sure we need most of these services, for a problem that may not even recur. However, the SO is kind of insecure about his lack of home maintenance expertise, as well as a fair bit more paranoid than me (his mind always goes to the worst-case scenario, which is great motivation for saving money, but fairly harrowing for everything else in life), so he feels better about being a bit more proactive rather than waiting and seeing and risking additional water damage.

He hired a gutter guy to replace the leaking gutters and add an extra downspout ($300). He also hired a landscaper to replace his hand-dug drainage ditch with a rock-lined dry creek bed ($900). He's also contracted with another landscaper to reslope the yard ($500) and reseed the lawn (that got torn up by the creek bed installation).

In addition to all of the above, he also wants to take down a dead tree that he's been eyeing for the past few years ($1000), and exterminate some carpenter bees ($200). Now he's also looking at window guys, because one of the windows seems to be rotting out a bit, and he's also considering hiring an asphalt guy to reseal the driveway ($850).

I am trying really hard to stay calm about this, because these are, by far, the largest expenses I've seen. On the other hand, I don't want the house to fall into disrepair, and I'm fine with hiring professionals to handle jobs we can't do on our own.

But we are feeling a little overwhelmed and in over our heads when it comes to dealing with the expense of home ownership and maintenance. I know we can technically afford everything, but is getting all this work done the right course of action? I guess you live and learn. This might be the one area where we will suck at conserving resources.

Posted in

Expense Log,

A Day in the Life,

Home ownership

|

8 Comments »

June 21st, 2014 at 03:12 am

Snapped a photo of my mpg gauge after this week's driving --

This is one of my best figures yet. Sometimes I feel like I over-purchased on my car, but fuel efficiency was my single most important criteria, and I've gotta say -- I'm pretty pleased that I can pull off gas mileages that are practically on par with hybrids.

Not only does it save on gas, but it also saves the planet!

Posted in

A Day in the Life

|

6 Comments »

June 19th, 2014 at 04:00 am

Here's an overview and analysis of all my financial accounts as of Wednesday, 18 June 2014 in excruciating detail.

CASH - $64,345

Yes, I know. I cringe when I look at this, because I know this is an absurd amount to hold in cash, but right now, I have $14,581 in my personal checking account, $7,873 in a joint checking account (the SO contributes his share of the mortgage here), $1,268 in a joint savings account, and $40,622 in my personal savings.

This is a somewhat hilarious "problem" to have, but I cannot get my cash levels down because I am hardwired to keep inflows greater than outflows, and it just keeps accumulating. I've been trying to move some of this cash into investments, but I wanted to dollar cost average rather than throw in a large lump sum (although I tried the latter too when I dumped $11K into an international stock fund last November). So I'm drawing down my checking account with weekly $400 automatic investments, but even with all of my other regular expenses (mortgage, Roth IRA, student loan and credit card payments) coming out of the same account, the balance isn't coming down. Actually, it's still going up. Sigh.

INVESTMENTS - $430,442

Here lie the bulk of my assets. My investments are primarily in retirement vehicles, but now that retirement is maxed, I'm redirecting excess cash to non-retirement brokerage accounts.

- 401(k)/403(b). My currently active 401(k) is at $82,419, and the 403(b) from my first job is at $13,847. The 403(b) is invested in the Vanguard Target Retirement 2050 Fund. The 401(k) is split 86.3% in Vanguard Institutional Index Fund Institutional Shares and 13.7% in company stock. I still need one more year to fully vest in the company stock match.

- Rollover IRA. The 401(k) from my second job is in a rollover IRA worth $42,250. I also have $8121 in stock match that's in a rollover IRA brokerage account. The non-stock portion is invested in Vanguard Target Retirement 2050.

- Roth IRA. The balance on my Roth IRA is $104,410. This includes a bit of rolled over Roth 401(k) from job #2. This is also invested in Vanguard Target Retirement 2050 (I'm apparently not very creative, okay??).

- Brokerage. I've got $47,766 in Vanguard 500 Index Fund Admiral Shares, $14,802 in Vanguard Total International Stock Index Fund Admiral Shares, and $14,265 in Vanguard Prime Money Market Fund, for a grand total of $76,834 in non-retirement investments. And yes, I know that Money Market is basically more cash. Ooops.

- Stock options. I have $102,296 in vested and exercisable stock options with my current company. I really don't know what to do with these. And here's the doozy -- I have an additional $142,396 in UNVESTED shares which is not included in this total. I feel like this portion of my net worth is actually cheating.

STUDENT LOANS - ($7274)

I still owe a little over $7K on my 3.5% Stafford loan. It started out at $17,125 in 2006, and I've got about seven years left on it. I've been known to chuck an extra hundred dollars at it every so often, but I'm not really in a hurry to pay it off.

MORTGAGE/HOUSE - ($1,516)

This one is a bit painful and not a success story. I paid $205K for my house in 2008, but it's current value on Zillow is only $136,621. I still owe $138,137 on the mortgage, which means that not only has it lost one-third of its value, I'm actually slightly underwater on the loan -- hence the negative sign. The one piece of good news was that I was able to refinance it through HARP last September to from a 30-year fixed rate of 5.875% down to a 15-year fixed rate of 3.875%.

My only other property is my car. It's a 2012 Civic that I bought last year to replace my dead 1999 Toyota Camry that I inherited from my dad. It was a bit more than I'd wanted, but I was on a short timeline because I needed a car to commute, and I was tired of having Roadside Assistance on speed dial. It's not financed so I own it outright, but I don't like counting it among the assets column because it depreciates, but Mint includes it under assets, so I guess it counts.

So that's everything. Here's what's on the to-do list for the moment.

Action item #1 - Fix the excess cash situation. Holy moly, this is clearly one area where I fail, and when I fail, I fail hard.

Action item #2 - Should I move the stock portion of the rollover IRA out? It's irritating to me for some reason. I guess I just don't like holding a single stock.

Action item #3 - Oy, how does one deal with all those stock options? They make the "you must diversify!" part of my brain hurt, but they're worth SO MUCH and WHAT IF IT KEEPS GOING UP. Should I buy them out and hold them for capital gains? I know nothing about stock options.

Action item #4 - The one constructive comment that I received from a consultation with two financial advisors two years ago was that my diversification is awful. Well, I had (and still have) no idea what I'm doing, so they're probably right. I really ought to figure out proper diversification and asset allocation.

Action item #5 - Should we accelerate mortgage payoff? I'm vaguely embarrassed that I'm underwater, but we do like the house and have no plans to sell. A paid-off house is still a paid-off house, right?

Posted in

Quantitate!,

Planning

|

4 Comments »

June 17th, 2014 at 10:55 pm

In honor of the relaunch of this blog, I am rechristening it! It's new name is Catching FIRE.

"FIRE" was an unknown term to me until recently. It all started when I was listening to an episode of Marketplace Money, and heard an interview with the man who runs the website, Mr. Money Mustache. That interview caught my attention because he described the simplest way I've ever heard to determine whether one can retire.

Take your annual spending, and multiple it by 25. If your retirement fund is worth at least that, then you're good to go. If not, you need to either save more or cut spending until you reach that magical 25 times or 4% ratio.

Curious, I tried it. Our current annual household spending is around $40K. Multiply it by 25, and you get one million dollars. With my net worth sitting at around half a million, and the SO's at around $400K...

Wait, what? Is it true that we're that close?! That can't possibly be! I know we're very good savers, but to be 90% of the way to retirement by age 30 is simply absurd. As they say in The Princess Bride, "INCONCEIVABLE!"

I've been saving for retirement since my first job out of college, but actual retirement has always been a very abstract concept because it was such a long way off. I knew that theoretically I should front-load retirement savings while time and the power of compounding was on my side, but I never thought I'd actually reap the fruits until decades later.

In The Millionaire Next Door, financial independence was defined as the ability to maintain one's lifestyle without working for a wage. While that sounded like an awesomely powerful achievement, most of the millionaires in that book were self-employed entrepreneurs. I knew that entrepreneurship wasn't really my style, so I figured that particular brand of financial independence was out of my reach. I'd have to run the traditional rat race, and just do the best that I can in that arena.

So I put my head down and plugged along, and resigned to continue plodding for the next three decades... until this 4% rule blew my mind out of the water. And after browsing on the MMM forums, I was introduced to the concept of FIRE -- Financially Independent, Retired Early -- and it all started to come together. You don't have to be a small business owner to achieve financial independence. All you need is to grow enough assets to generate the cashflow required to support your living expenses. That's not rocket science. I mean, I can do that.

All of a sudden, financial independence and retirement went from a dreamy and remote "someday" to concretely achievable in the not-so-distant future. And what an awesome, dream-come-true achievement that would be. Rather than some abstract and impossibly far away concept, I have a solid goal to plan and strive for now.

We're gonna catch some FIRE.

Posted in

Musings

|

4 Comments »

June 17th, 2014 at 04:27 am

I was reading back over some of my old entries, and discovered that in 2006, my net worth was $5K.

Today, my net worth is around half a million.

That's two orders of magnitude increase in eight years. Whoa.

Granted, my salary did almost triple between then and now, which is very helpful. And I've always tried to keep expenses low, so I can save more of my income. And I've had help -- ever since my SO moved in, we share expenses and live very efficiently.

But I must also point out that I haven't actually been trying to grow my wealth. All I've been doing is maxing out my retirement accounts, and auto-investing in some index funds. It's all very passive, autopilot, set-it-and-forget-it style investing. Aside from logging into my checking account to pay off my credit cards every month, I can go months without checking my other financial accounts.

A few months back, though, I logged into mint.com, and noticed that my net worth topped half a million. I was in total shock. That was a huge milestone.

I am well-aware that in recent years, the stock market has been going gangbusters, which obviously contributed to the exponential growth of my net worth -- a pattern which will likely not hold forever.

But it also made me acutely aware that the playing field has now fundamentally changed.

Instead of generating wealth by saving income and watching those savings accumulate in a linear fashion, I now release those savings into the market, for it to do what it will. Instead of having savings be the main driver of increases in wealth, market appreciation is now the primary source of the (exponential) increases (or decreases!) in wealth. It's an entirely new paradigm, and it is a little frightening.

This is why I need to learn more than just how to play good defense -- or even offense; my salary is not going to triple again. I need to learn how to manage and balance investments, because that is the only path forward. I guess I'm in the big leagues now. Gotta step up and own it. Or at least try.

Posted in

Quantitate!,

Musings

|

6 Comments »

June 17th, 2014 at 12:00 am

It's been a while, but I am back, and I am rebooting O Capitalism!

When I started this blog back in 2006, I had just graduated from college, and was starting to work through the ins and outs of being on my own. After figuring out the basics of frugal living and financial management (including the magic of compounding interest), and especially after landing a terrific new job, I sort of went on autopilot for a while, and stopped thinking about and working at personal finance.

However, a lot has happened over the past six years, and here's the whirlwind cliff notes version. After changing jobs, I bought a house (2008), my SO moved in (2009), we got some cats (2009, 2010), I lost my job (2011), I earned a Master's degree (2011), I found a new job out of state (2011), I paid off one of my student loans (2011), I replaced the 14-year-old car I inherited from my parents (2013), I refinanced my mortgage (2013), and that brings me to now.

This year, 2014, I am turning 30. It's hard to believe that time has flown so fast, but I am officially bidding good-bye to my 20s and young adulthood. I feel like I need to reassess where I've been, where I'm going, and plot a fresh new course for the next decade. After all, this is a long game.

Let's play.

Posted in

Musings,

Planning,

A Day in the Life

|

0 Comments »

March 23rd, 2008 at 04:59 pm

I've been sitting here, trying to decide how to portray this past year, whereby I transformed from a bright-eyed and bushy-tailed academic wannabe to, well, a corporate whore.

For anyone in biomedical research, especially in academia, the Text is funding situation and Link is http://scienceblogs.com/transcript/2006/07/nih_funding_stagnates.php funding situation is getting dire as NIH grants become more and more scarce. Labs, including my own at Yale, were running out of money, and new grant applications still get continually rejected. My PI's (principle investigator, also known as the boss or head of the lab) attempt to solve this problem involved hiring more postdocs, and pushing his staff as far as they can stand, and then some, to try to eke out the publications that the lab needs to renew existing grants and land new ones.

I don't think anything has shaken my faith in science more than reading and generating data for my PI's grant applications. I'd do the experiment once, and get a small positive effect. I'd repeat it, and get a small negative effect. The third time is the charm, and will finally answer the question, right? Nope, the third result is *no* effect.

If I had to draw a conclusion, it would be that there is no effect. What ends up happening? The PI grabs the result that fits with his hypothesis, plops it into the grant application like it is fact, and pretends that the other two results don't exist.

Meh?

I've heard the justification. "We must put our best foot forward in the grant application to get the money FIRST, and then we can explore the complexities in greater detail AFTER," he explained. Um, okay. That's great and all, but if your hypothesis is WRONG, or even seriously flawed, you won't be able to publish those coveted Shiny Papers In High-Impact Journals, even if you get the money.

Right? Or am I missing something here?

And then there were my PI's ill-conceived attempts to save money, like giving every lab member a monthly budget for their experiments. Now I take care of keeping the lab stocked with "common" lab supplies, while the other lab members ordered the specific reagents they needed for their own experiments. But after the budget got imposed, everyone was afraid of ordering reagents and spending money, so they all ended up coming to me and asking me to order their reagents for them, since I'm "in charge of ordering stuff"; but really, they just wanted my name on the bill instead of theirs. In fact, in the weeks prior to my departure, I was informed that members of the lab were specifically saying amongst themselves, "Oh, X, Y, and Z reagents are expensive, but we need them for the experiment! We must make Mimi order then before she leaves!"

I could go on and on about how the budget crunch, and my PI's clear inability to effectively manage his funds and his staff, sent everything into a downward spiral, but I'll spare you the grisly details. Let's just say that I grew increasingly bitter, disheartened, and I completely burnt out.

By the summer of 2007, I was already sending out e-mails and scoping out new jobs. I got my driver's license, moved in with my boyfriend, and started carpooling to work so that it forced me to adhere to a consistent work schedule, rather than pouring in countless hours of unpaid and thankless overtime. I also enrolled in culinary arts classes at a local community college, because all I could think about at work was how much I'd rather be cooking at a restaurant. It's the same kind of manual labor, minus the biohazard.

I got a break during November, when attending a conference. (Me and three other postdocs crammed ourselves into a tiny motel room for five days to cut expenses. After that experience, we vowed never to do that again. Two guys, two girls, two bed, and one smoker did not a pleasant experience make.) I found out that a major pharmaceutical company in the state was hiring. Immediately, I sent in my resume.

The Monday before Thanksgiving, my PI comes into the office while I'm alone (I'm always the first one in, so he knows when he can find me alone), and asks me "what my plans are". I answered in the usual fashion, that I was going to stay until next summer, and then move on to industry. He replies that the funding situation is bad, and that I should start looking for jobs as soon as possible; the job market's not great, it may take me eight months to find something; I should even consider looking out of state! But, if I do get an offer, they'll probably want me to start right away, so I can leave earlier than next summer if I want to. Even next February!

Hint hint.

My PI can be incredibly passive-aggressive and manipulative, I can recognize a layoff warning when I hear one. Lovely. Maybe it's because he found out that I was no longer working 15 hours a week in overtime, thanks to my need to catch my carpool? Or that I was taking culinary classes, which had nothing to do with the Lab To Which Everyone Must Devote Their Entire Being? Or that my name is associated with all the major lab supplies expenditures? Or did he just choose me because I was the only staff without a family, and had the best chance of landing another job? Or because he knew I'd planned on leaving anyway? It didn't matter. It was done.

(Did I mention he had this talk with me the Monday before Thanksgiving? I had a really crappy Thanksgiving.)

But then, in December, I got a call back from Major Pharmaceutical Company. They wanted a phone interview! And then they wanted an in-person, on-site interview! I went out and spent $250 on an interview outfit, including $150 at a specialty shoe store on the only pair of shoes that fit me that I found acceptable. (As it turned out, I'm a size 4.5. Department stores don't even carry below a size 6, so I had to go to a specialty shoe store and pay the premium.)

The day after my interview in mid-December, I get a phone call. They're making me an offer! And paying me $10,000 more than I'd asked for.

I had a good Christmas.

I told my PI of my job offer in January, and gave him my two weeks. I could tell by his body language that he was surprised and even dismayed that I would be leaving so soon (it kind of figures that he realizes at that particular moment that I am not, in fact, easily dispensable), but I insisted that my new job wanted me to start as soon as possible, and I would be taking a week off between jobs (the ONLY time I have EVER taken off), and two weeks was all that he was going to get.

My PI completely avoided me my last two weeks. He didn't attend my farewell lunch. I couldn't even find him on my last day to say goodbye.