|

|

|

Viewing the 'Quantitate!' Category

May 21st, 2015 at 04:38 am

It tools weeks of wrangling, but multiple calls and e-mails to multiple insurance companies have paid off.

Last year, my homeowner's and auto insurance premiums were:

- home: $1031

- car #1: $1233 (comprehensive)

- car #2: $630 (liability)

- total: $2894

Now, after raising deductibles and lots of relentless haggling back and forth, I've gotten them reduced to:

- home: $676

- car #1: $620 (still comprehensive!)

- car #2: $267

- total: $1563

So I just saved $1,331 per year. Not bad at all. Between this and the $2715 savings in health insurance premiums when the SO and I both switched to high-deductible health plans, and this is a good year for insurance. Probably should have done this sooner, in retrospect, but from now on, I'm gonna keep a much closer eye on the insurance bill -- because jousting with insurance agents could be way worse.

Posted in

Quantitate!,

Groceries & Bills,

Home ownership

|

2 Comments »

April 13th, 2015 at 01:33 am

Posted in

Quantitate!

|

2 Comments »

April 10th, 2015 at 08:51 am

Quick snapshot of the financial situation as of close of business 9-Apr-15:

Cash: $16,297.63

Home: $169,378 minus ($129,766.66) mortgage = $39,611.34 equity

Car: $13,900

Investments: $749,901.40

- 401(k): $113,746.98

- Roth IRA: $115,696.03

- Rollover IRA: $65,449.31

- Rollover IRA Brokerage: $9818.84

- HSA: $1132.78 (currently in cash; need $2500 minimum balance to invest)

- Taxable: $149,983.61

- Stock Options: $294,073.85 vested (out of $504,931.90 total)

Net Worth: $819,710.37

In recent weeks/months, I've made the following adjustments to my portfolio:

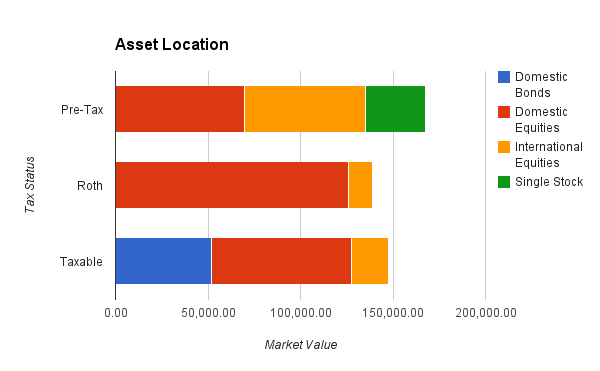

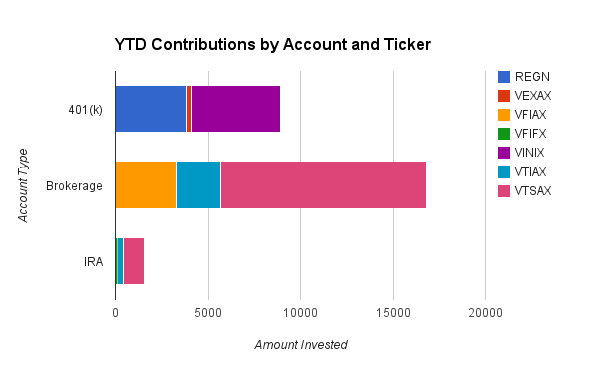

- Swapped 20% of my 401(k) from Vanguard Institutional Index (VINIX) to Vanguard Extended Market Index (VEXAX) to approximate the Vanguard Total Stock Market Index (VTSAX, which I can't get directly in my 401(k)), and balanced my future contributions to be an 80/20 split.

- Seeded $11K from money market into a taxable VTSAX holding, and will henceforth be using that instead of my S&P500 holding, which I'm retiring.

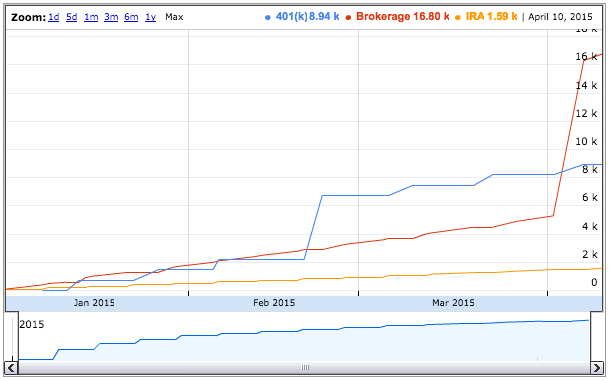

- Increased my taxable investments from $400/week to $500/week -- because I got a raise and bonus at the end of last year, and what else am I gonna do with it? :P

- Killed my (brand-new  ) traditional IRA. I apparently make too much money to take the deduction now. ) traditional IRA. I apparently make too much money to take the deduction now.

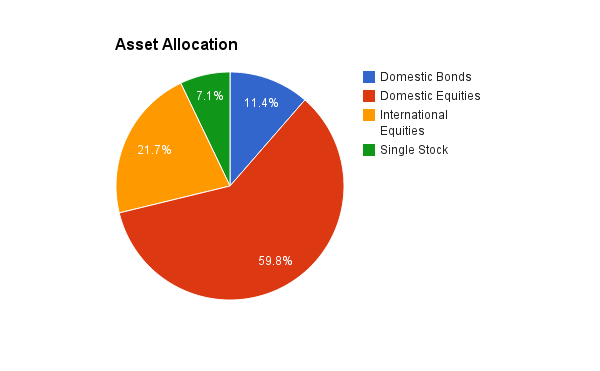

- I want my domestic to international equities ratio to be 2:1, but I'm at 2.76:1 right now, so I'm aggressively rebalancing my AA more towards international without triggering taxes. All of my Roth IRA and 80% of my taxable contributions are going towards Vanguard Total International (VTIAX). If this approach is taking too long (e.g. if by next quarter that ratio has barely shifted), I might buy/sell within my Roth space, or rebalance my 401(k) contributions.

I set a goal in Mint where I called reaching $1M in assets (excluding home/car equity and HSA) "FIRE", and the projected completion date is sometime in 2017 (April 27 at the moment, but it jumps around a lot). I love the fact that market appreciation is actually dwarfing my (fairly substantial) monthly contributions. Go Go Gadget Compound Interest!

Posted in

Quantitate!,

Early Retirement,

Investing

|

2 Comments »

March 27th, 2015 at 05:15 am

The SO and I have finished our tax returns for 2014. Just for funsies, we ran the numbers to see what our taxes would look like if we were to get married.

The results were NOT pretty. Essentially, my income would push him into a higher tax bracket that would nix his traditional IRA deduction, and his standard deduction would nix my itemized [mortgage interest] deduction... and we'd wind up paying an extra $2822 in federal taxes every year. It does not matter if we file jointly or separately -- the two are within six dollars of each other.

Even taking into account the savings of putting him on my employer health plan, marriage would still be a major net loss financially (and I'm not sure if spouses get their own HSA match). We don't have (nor do we ever want) kids, so that issue would does not apply, and other quantifiable benefits (like the spousal estate tax deduction) only apply if one of us dies. And in the case of my untimely early demise, I'd much rather leave my assets (with the exception of the house) to my parents anyway, since they need and deserve it way more.

Social Security is another consideration, but that won't be relevant for a while. And you only need to be married for one year to get spousal benefits, so there's no rush unless someone is actually dying (and I suspect if we're still together three decades from now that we'll be married by then anyway).

So what would it take for the marriage penalty to go away? Paying off the house would get rid of the itemized mortgage interest deduction for me, and the SO could get enough salary increases to phase out of the traditional IRA range all by his lonesome. We might hit the Roth IRA phase-out range faster if married, but I think that possibility is a more remote one due to how high that threshold is.

Joint high(er) incomes don't scale favorably regardless, but if I quit my job (due to achieving FIRE) and my earned income drops, then marriage could turn beneficial if we live off his income alone... but we'd have to run the numbers if I want to employ tax strategies like Roth conversion ladders. If we both FIRE on combined assets, then income would be too low trigger the penalty.

But in the current situation, I can only come to the conclusion that it makes NO sense to get married. I really want to at the very least break even. I realize that this is horribly unromantic, but this is just the way my mind works. I'm relentlessly rational, and the SO is similar, so we fit.

The next time my father nags me about not being married, maybe I'll just ask him to pay me three grand a year. That'll probably shut him up!

Posted in

Quantitate!

|

2 Comments »

October 2nd, 2014 at 12:12 pm

Up until now, I've been using Roth IRAs exclusively. I just followed the extremely typical advice for young people to use a Roth, because it's better to pay taxes when one is younger, making less income, and thus in a lower tax bracket.

I also thought that the math worked out better, at least if one assumes a constant tax bracket. In a Roth, you pay your taxes up front, but everything after that grows and is withdrawn tax-free. It's a very simple FV calculation. In a traditional IRA, the same contribution amount goes in and grows tax-free, so you wind up with the same FV as the Roth, but the withdrawal is taxed.

This seems like a bad deal until you remember that you get to keep the taxes that you would've lost with the Roth. If you also invested the amount that you would've paid in taxes, and let that grow over time, it essentially makes up for the withdrawal taxes on the IRA itself, at least if the tax rate is the same. However, that investment with the saved taxes is outside of the IRA, so it is not tax-advantaged, so you actually wind up with less FV than if you'd just gone Roth to begin with.

So I managed to think through all of that, but for some reason, I never questioned the implicit assumption that my tax bracket in retirement would be the same as now (or higher). I guess I wanted to make sure that I "could" withdraw as much as I wanted in retirement, so I didn't see the harm in accepting that I'd have a high income in retirement.

Now that I'm properly thinking through my current income and expenses, it has become abundantly clear that this assumption is false. My savings rate is in excess of 50%, so I am spending nowhere near my current level of income, and my expenses are expected to drop even further once the mortgage is paid off. There is ZERO need for me to replace my current income, so I will be in a LOWER tax bracket in retirement -- and that's a good thing, because it makes FIRE that much easier to achieve.

So it seems like Roth has been the wrong way to go all along. I should've been using a traditional IRA and taking the tax break right now. Oh well.

I've gone and made myself a traditional IRA in Vanguard, and I'm swapping over to it. I may even inquire about recharacterizing this year's contributions. This just goes to show that always assuming a worst-case scenario can cost ya.

(I also have another reason why I'm interested in switching to traditional, and that has to do with the Roth Conversion Ladder, which I'm learning about right now. Maybe I'll write it about it later, after I've got it worked out in my head.)

Posted in

Quantitate!,

Planning,

Early Retirement

|

2 Comments »

September 27th, 2014 at 09:28 pm

I realize that pensions are rare like unicorns these days, but I actually have a small one under a previous employer. It's not worth much because I only worked there for three and a half years before being laid off, but the pension is supposed to pay out $261.88 per month starting in 2049 (when I turn 65).

They are now offering what I presume is a buyout. I can either:

1. Roll over a lump sum to an IRA or another employer's qualified plan ($6352.78).

2. Take a lump sum cash distribution ($5082.22).

3. Start monthly payments now ($24.71).

4. Retain the original pension benefit.

Should I take it? To figure out if this is a good deal, I calculated the present value of this future annuity.

Step one: Calculate the PV of the annuity at age 65. I'm arbitrarily using an interest rate of 6%, and a life expectancy of 100 (so 35 years).

PV(0.06/12,12*35,261.88) = $45,928.57

Step two: Discount that to today's dollars using the same rate.

PV(0.06,2049-2014,0,45928.57) = $5975.55

So it looks like the lump sum payment is a reasonable offer. I'm also assuming an extremely long life expectancy, which would bias the value upward. I'm not sure what rate I should use, but 6% is a figure I can hope to beat by investing on my own. I've tried plugging in different interest rates, but that causes the PV to fluctuate wildly.

I am really tempted to take it. If I roll it into an IRA now, I know I'll have control of and access to it before age 65, which is particularly helpful if I'm planning ER. I also avoid the risk of the company underfunding, raiding, or otherwise reneging on their obligation (I'm looking at you, Hostess) anytime in the next 35 years. I have so far been completely ignoring my pension in retirement planning, so this would allow me to take it into account.

I have until month's end to decide. Hmm.

Posted in

Quantitate!,

Planning,

Early Retirement,

Investing

|

9 Comments »

September 12th, 2014 at 12:45 pm

I recently compiled a somewhat exhaustive record our household's monthly and annualized expenditures, I thought I'd share it on the blog.

Housing - $20,739

The mortgage, at $1377/mo or $16,519/yr, is the biggest housing expense, and it includes $2600 property tax and $1031 in homeowner's insurance. I work out-of-state, two hours away from home, so I also rent a room near work where I stay during the work week, which comes out to $310/mo or $3720/yr. I also budget in $500 for various DIY projects such as deck staining and weed whackers.

This is by far the largest part of our annual expenditures, and I’ll talk more about it at the end.

Utilities - $1760

Electricity usage per month is around 320 kWh, which comes out to $60/mo. Water usage is typically 100 cubic feet, or $20/mo. Internet (cable modem) is $30/mo. We don't have (nor do we want) cable TV. Trash and recycling pickup is $20/mo. Cellphones are currently free, because the SO gets reimbursed by his employer and I'm mooching off my parents' plan. Heating oil is spiky and my records aren't great because the SO orders the oil, but I'm guestimating it's about $200/yr.

I'm using long-term (two year) averages for the utility figures, so I think they're fairly accurate. Heating oil is the only exception, because that is highly dependent on the price of oil and the winter weather, but we already keep the thermostat in the low 50s so there’s not much more that can be done there anyway. The only area we might be able to reduce is trash pickup, because we don't generate enough trash to need weekly pickup, but my address is not allowed to use the dump, so I'm kind of stuck hiring a service. If there's no cost to cancelling and resubscribing, I might just sign up for a month of trash pickup a few times a year, but I'd have to look into that.

Automotive - $5413

Currently, we have two cars. Mine is 2 years old, the SO's is 14 years old, and both are paid off. Insurance is costing $1233/yr for comprehensive collision for my car, and $630/yr on liability for his. My maintenance costs are $120 for 2 oil changes per year, but the costs on the 14-year-old car are much higher; maybe $1200 or so? I haven’t really been tracking his car repair expenses, but I'm gonna try to start doing that now. As for gas, mine is around $1300. I have no idea what the SO spends on gas, because he rides in a carpool most of the time and he doesn't track his fill-ups as maniacally as I do, but since he does all the local driving to the grocery stores, I’m guestimating it at $600/yr.

In some ways, cars are a discretionary cost, but we're in a small town, and a car is our primary means of transportation. I have done the research on the public transport options in the area, and it is wildly inconvenient to go to the grocery store or the dentist's office by bus. We also travel regularly to see family out-of-state, and while it's possible to make the trip on public transportation, it was time-consuming and not fun at all. There is also the issue of potential emergencies, like rushing the cat to the vet. At the end of the day, we think it is worth it to spend the money for the convenience of having a car.

With that said, I would love to drop down to a single car in the future. A used but not-too-crappy car would keep both amortized costs and insurance low. Aside from the work commute and grocery runs, we don't drive much anyway, so if I can ditch my commute, I don't think we'd still need two cars. That would save a few grand a year.

Medical - $4682

The SO and myself both get medical and dental insurance through our work. Our health premiums are $1690/yr (me) and $2513/yr (SO), and our dental is $156/yr, and $224/yr. I also threw his $100 annual deductible into the budget, but I haven't been to a doctor in 7 yr (I know! I’m terrible! I better not have cancer). It's kind of sad, how different our health plans are, because even if the SO switched to a high-deductible HSA-eligible plan, his annual premium would still be $1844, which is higher than my normal plan, but it's actually a fair price for insurance.

I half-joke that we should get married just so I can put him on my health plan and save almost $1000 a year. Even taking into account the amount we'd spend on a wedding, we'd break even after a year or two, heh.

Consumables - $5100

This category encompasses all the regular, discretionary but non-emergency spending, including food and entertainment. The figure that drove the last financial advisor crazy was the $160/mo ($1920/yr) I put down for groceries. Yes, that's what we spend, and no, we don't live on ramen (unless it’s homemade, delicious ginger tempeh soup with ramen and bok choy). I don't really dine out either, because unless I'm in a college town or a specialized restaurant, the vegetarian options tend to be either nonexistent or wholly uninspired. The SO does spend $40/wk going out to lunch, but that is how he pays for his carpool, so it should probably count towards the transportation budget. Between these two items, that’s $4000/yr.

Aside from food, the rest of the discretionary budget covers entertainment (generally either Netflix or various video games), pets, and odds 'n ends such as gifts and other miscellaneous purchases. The most costly indulgence is the Broadway tickets we get once a year, but aside from that one night out, I prefer staycations to vacations. All of those total no more than $1000/yr.

Total - $37,695

One-Time Large Expenditures - ???

We do encounter occasional, isolated, large expenditures which I’m not including in the regular budget, but we do have to take into account. Last year, I traveled to California for a wedding, and we had veterinary emergency, all of which cost more than $3000. This year, housing maintenance is shaping up to be the big unanticipated expense.

ANALYSIS

So housing takes up the bulk of annual expenditures. Paying off the mortgage alone would drop expenses down to $25K. If I'm no longer renting and driving out-of-state, that would chop off another $5K, and would drop annual expenditures down to $20K. Most of the other categories, such as utilities and medical/dental premiums, are fairly inelastic. We definitely need both cars right now, but maybe we won't in the future. There isn't much fat to trim in consumables, either.

At our current expense level, I would have to bring in $40K / 2 = $20K to maintain our lifestyle. After the mortgage is paid off, I'd only have to bring in $10K to $13K. Obviously this may change, but I am wracking my brain for what I might want to spend more on, and I'm honestly drawing a blank. I’ve never been big on consumerism, and the only areas where I enjoy spending money is food/cooking and pets. And the pets kind of prevent me from being able to have nice things anyway, because it's all just gonna get shredded by sharp (but adorable!) claws and teeth.

What's way more important to me than planning for possibly higher future spending is making sure that I can be fully independent without the SO -- because he might get run over by a truck tomorrow (yes, that is how my mind operates). That means being able to handle the doubling of all expenditures. This is absolutely essential to my peace of mind, and will likely result in a ton of overcompensation in retirement planning/projections, but I'm okay with that. At the end of the day, I'm the only one that I can truly count on.

Posted in

Quantitate!,

Expense Log,

Planning

|

3 Comments »

July 1st, 2014 at 07:27 pm

I adore watermelon -- it is one of my favorite fruits. I'm generally not a big fan of summer (too hot, and sweating is gross), but one thing I do look forward to is watermelon.

This week, one of the loss leaders at my local Stop 'n Shop was a whole watermelon for $3.99.

I picked through the bin, tapping and weighing each one, until I found a behemoth that clocked in at 20.62 lbs.

Afterwards, I ran the math -- $3.99 / 20.62 lb = $0.19 per lb

Hee! I am very pleased with myself.

Posted in

Quantitate!,

Groceries & Bills,

A Day in the Life

|

2 Comments »

June 19th, 2014 at 04:00 am

Here's an overview and analysis of all my financial accounts as of Wednesday, 18 June 2014 in excruciating detail.

CASH - $64,345

Yes, I know. I cringe when I look at this, because I know this is an absurd amount to hold in cash, but right now, I have $14,581 in my personal checking account, $7,873 in a joint checking account (the SO contributes his share of the mortgage here), $1,268 in a joint savings account, and $40,622 in my personal savings.

This is a somewhat hilarious "problem" to have, but I cannot get my cash levels down because I am hardwired to keep inflows greater than outflows, and it just keeps accumulating. I've been trying to move some of this cash into investments, but I wanted to dollar cost average rather than throw in a large lump sum (although I tried the latter too when I dumped $11K into an international stock fund last November). So I'm drawing down my checking account with weekly $400 automatic investments, but even with all of my other regular expenses (mortgage, Roth IRA, student loan and credit card payments) coming out of the same account, the balance isn't coming down. Actually, it's still going up. Sigh.

INVESTMENTS - $430,442

Here lie the bulk of my assets. My investments are primarily in retirement vehicles, but now that retirement is maxed, I'm redirecting excess cash to non-retirement brokerage accounts.

- 401(k)/403(b). My currently active 401(k) is at $82,419, and the 403(b) from my first job is at $13,847. The 403(b) is invested in the Vanguard Target Retirement 2050 Fund. The 401(k) is split 86.3% in Vanguard Institutional Index Fund Institutional Shares and 13.7% in company stock. I still need one more year to fully vest in the company stock match.

- Rollover IRA. The 401(k) from my second job is in a rollover IRA worth $42,250. I also have $8121 in stock match that's in a rollover IRA brokerage account. The non-stock portion is invested in Vanguard Target Retirement 2050.

- Roth IRA. The balance on my Roth IRA is $104,410. This includes a bit of rolled over Roth 401(k) from job #2. This is also invested in Vanguard Target Retirement 2050 (I'm apparently not very creative, okay??).

- Brokerage. I've got $47,766 in Vanguard 500 Index Fund Admiral Shares, $14,802 in Vanguard Total International Stock Index Fund Admiral Shares, and $14,265 in Vanguard Prime Money Market Fund, for a grand total of $76,834 in non-retirement investments. And yes, I know that Money Market is basically more cash. Ooops.

- Stock options. I have $102,296 in vested and exercisable stock options with my current company. I really don't know what to do with these. And here's the doozy -- I have an additional $142,396 in UNVESTED shares which is not included in this total. I feel like this portion of my net worth is actually cheating.

STUDENT LOANS - ($7274)

I still owe a little over $7K on my 3.5% Stafford loan. It started out at $17,125 in 2006, and I've got about seven years left on it. I've been known to chuck an extra hundred dollars at it every so often, but I'm not really in a hurry to pay it off.

MORTGAGE/HOUSE - ($1,516)

This one is a bit painful and not a success story. I paid $205K for my house in 2008, but it's current value on Zillow is only $136,621. I still owe $138,137 on the mortgage, which means that not only has it lost one-third of its value, I'm actually slightly underwater on the loan -- hence the negative sign. The one piece of good news was that I was able to refinance it through HARP last September to from a 30-year fixed rate of 5.875% down to a 15-year fixed rate of 3.875%.

My only other property is my car. It's a 2012 Civic that I bought last year to replace my dead 1999 Toyota Camry that I inherited from my dad. It was a bit more than I'd wanted, but I was on a short timeline because I needed a car to commute, and I was tired of having Roadside Assistance on speed dial. It's not financed so I own it outright, but I don't like counting it among the assets column because it depreciates, but Mint includes it under assets, so I guess it counts.

So that's everything. Here's what's on the to-do list for the moment.

Action item #1 - Fix the excess cash situation. Holy moly, this is clearly one area where I fail, and when I fail, I fail hard.

Action item #2 - Should I move the stock portion of the rollover IRA out? It's irritating to me for some reason. I guess I just don't like holding a single stock.

Action item #3 - Oy, how does one deal with all those stock options? They make the "you must diversify!" part of my brain hurt, but they're worth SO MUCH and WHAT IF IT KEEPS GOING UP. Should I buy them out and hold them for capital gains? I know nothing about stock options.

Action item #4 - The one constructive comment that I received from a consultation with two financial advisors two years ago was that my diversification is awful. Well, I had (and still have) no idea what I'm doing, so they're probably right. I really ought to figure out proper diversification and asset allocation.

Action item #5 - Should we accelerate mortgage payoff? I'm vaguely embarrassed that I'm underwater, but we do like the house and have no plans to sell. A paid-off house is still a paid-off house, right?

Posted in

Quantitate!,

Planning

|

4 Comments »

June 17th, 2014 at 04:27 am

I was reading back over some of my old entries, and discovered that in 2006, my net worth was $5K.

Today, my net worth is around half a million.

That's two orders of magnitude increase in eight years. Whoa.

Granted, my salary did almost triple between then and now, which is very helpful. And I've always tried to keep expenses low, so I can save more of my income. And I've had help -- ever since my SO moved in, we share expenses and live very efficiently.

But I must also point out that I haven't actually been trying to grow my wealth. All I've been doing is maxing out my retirement accounts, and auto-investing in some index funds. It's all very passive, autopilot, set-it-and-forget-it style investing. Aside from logging into my checking account to pay off my credit cards every month, I can go months without checking my other financial accounts.

A few months back, though, I logged into mint.com, and noticed that my net worth topped half a million. I was in total shock. That was a huge milestone.

I am well-aware that in recent years, the stock market has been going gangbusters, which obviously contributed to the exponential growth of my net worth -- a pattern which will likely not hold forever.

But it also made me acutely aware that the playing field has now fundamentally changed.

Instead of generating wealth by saving income and watching those savings accumulate in a linear fashion, I now release those savings into the market, for it to do what it will. Instead of having savings be the main driver of increases in wealth, market appreciation is now the primary source of the (exponential) increases (or decreases!) in wealth. It's an entirely new paradigm, and it is a little frightening.

This is why I need to learn more than just how to play good defense -- or even offense; my salary is not going to triple again. I need to learn how to manage and balance investments, because that is the only path forward. I guess I'm in the big leagues now. Gotta step up and own it. Or at least try.

Posted in

Quantitate!,

Musings

|

6 Comments »

December 6th, 2006 at 05:45 am

I spent all of this evening attempting to track, once and for all, every single penny that came into and out of my stewardship since June 12, the day I moved to this fine town and started my job.

Through this process, I discovered a few things.

One. I may not throw out any of my receipts, but I sure as hell can't FIND all of them. FRUSTRATION.

Two. I was missing over a grand in net pay, until I finally figured out that I never cashed a paycheck of mine, issued back on August 3. I cannot for the life of me locate said paycheck. DEFINITELY CONTACTING PAYROLL ON THE MORROW.

Three. I also never cashed a $400 deposit check that was returned to me when I vacated my summer sublet housing. Oops.

Four. The fact that my credit card posts transactions two days after the fact is very, very annoying, especially when it doesn't match the receipts I have.

Here are some random stats:

- Net income: $10,283.80 (this includes the missing paycheck)

- Total spending: $4727.22 (this includes the $400 deposit)

- Roth IRA contribution: $2203.33

- 403(b) contribution: $998.41

- Targeted savings: $2440

My pattern of spending:

- Public transportation: $93.5 (mostly to visit the BF)

- Groceries: $409

- Student loans: $401.16 (repayment started in September)

- Housing: $3275 (includes $400 deposit that I should have gotten back, plus $1000 deposit that I get back later)

Damn is housing pricey!

I really, really hope I can call up the subletters and have them rewrite my deposit check. Sigh. I need to get better about depositing checks. Gah.

I also need to get my free annual credit report thingy. Running out of time for that one!

Posted in

Quantitate!

|

2 Comments »

October 13th, 2006 at 08:32 am

Just for fun, I crunched the numbers on my Roth IRA, which is invested in Vanguard's Target Retirement 2050 Fund.

Since 8/31, I have invested a total of $7,031.72.

As of today, my Roth is worth $7,284.21.

That's a 3.59% growth in the past 1.5 months, or a monthly growth rate of 2.39%.

Extrapolate this out to a year, and that's an annual growth rate of 28.7%.

If I calculate just by share price, the growth rate becomes 29.9%.

Is this for real??

I'm sure that the growth rate won't actually hit this obscenely high figure, and average annual growth rate will actually end up being more in line with the other Target Retirement funds at 12% to 13%.

But it's still nice to dream.

And my father has started asking me for investment advice, since his retirement fund isn't doing nearly so well (it's actually losing money). ME! And he asked me about variable annuities, and I actually told him some info on those that he didn't know before.

*scurries off to continue reading Business Week Guide to Mutual Funds*

Oy, what is the world coming to??

Posted in

Quantitate!

|

2 Comments »

September 27th, 2006 at 08:14 am

The SO finally called the bus company to inquire about commuter discounts for the bus between New Haven and Middletown.

(52 weeks/year) * (5 weekdays/week) / (12 months/year)

= 21.67 weekdays/month

=~ 22 weekdays/month

At the standard fare of $3.60 per way, that's $158.40/mo

There is a 10-ride discount fare of $32, or $3.20 per way, or $140.80 per month.

There is also a monthly pass for $122.

This decreases the estimated monthly car maintenance cost to $200 to $250 per month.

Sweet.

Posted in

Quantitate!,

Planning

|

0 Comments »

September 18th, 2006 at 11:10 pm

Goal: bump myself down to the lowest federal income tax bracket through my 403(b) deduction.

Gross income this year from current job: $17,617.25.

Add in work-study and round up a bit: $17,850.

Exemptions:

- $5150 (standard single)

- $3300 (personal, non-itemized)

Taxable income after exemptions: $9400.

Total 403(b) deductions: $1865.33.

Taxable income after 403(b): $7534.67.

Lowest federal income tax bracket: $7550 or below.

Wow, that's really kind of cutting it close. Especially since my math kind of gets fuzzy at certain points.

Maybe I should up my deduction.

As for income taxes, I've already had $1407.97 withheld from my paycheck this year to date. 10% of $7550 is $755.

Yes, definitely no more taxes this year.

Posted in

Quantitate!

|

1 Comments »

September 11th, 2006 at 04:13 am

I've gone and made a spreadsheet projecting my retirement fund from now until 2049, which is when I'm 65.

Voila! (Link must be opened in Firefox 1.5+ or Internet Explorer 6.)

I'm assuming an average annual rate of return of 8%.

I plan on maxing out my Roth IRA every year until I retire, including my grad school years, if they come to be. I know max contributions will rise, but I just kept it at $4000/year since I don't know when it'll rise, or what it'll rise to.

I also plan on contributing $10K/year to my 403(b) for the next two years, and $15K/year for the following two years, and then stopping (for grad school?). I don't pick it back up at all in this set of projections, although I probably will in reality.

At the end of 2049, I will have earned $1.88 million tax-free dollars from my Roth from an input of $184,377.96.

I will have over $900.000 in my 403(b) from a total input of less than $35K.

The net worth of my retirement fund at 2049 will be $2.79 million.

Someone please pinch me?

Posted in

Quantitate!

|

4 Comments »

September 10th, 2006 at 04:28 pm

Repayment starts today on my $17,125 Stafford principal. (My Perkins is still in grace.)

I gotta crunch the numbers to figure out whether I should accelerate repayment.

Mind you, I may not currently have the funds to accelerate repayment even if it turns out to be advantageous, but it's still an interesting exercise to go through. While I do find it psychologically painful to be in debt, I'll stick with debt if the numbers show that it actually helps my bottom line.

As it turns out, there's no clear-cut BETTER. It all depends on how you work the situation. But let me start at the beginning, with the background on my Stafford loan.

I owe a principal of $17,125. I consolidated the interest rate at 4.75% at the end of June, and got it reduced to 4.5% by activating auto-debit. After 36 on-time payments, my interest rate drops another percentage point, to 3.5%. I do intend on this happening, since I've got the auto-debit.

I'm on the standard/level repayment schedule, which is 180 months, or 15 years. My monthly payment is $133.72. Taking the two interest rate drops into account, I'll actually pay the loan off in 176 months.

If I pay nothing but the minimum for the entirety of the 176 months of repayment, I'll pay a total of $6360.52 in interest over the life of the loan.

But say I up my monthly payment to $200, which means I pay an extra $66.28 towards my principal per month. The repayment period drops to 104 months, or 8 years and 8 months. For the extra $6870.51 I pay over those 104 months, my total interest paid gets reduced to $3652.39, for a savings of $2708.13.

But I also ran a parallel calculation, where I take the extra payment amount of $66.28, and invested it instead. Over the course of 104 months, I'll earn more money from the investment, so long as the fund's rate of return exceeds 7.35312%. If the stock market gives a long-term average return of 8%, I'll earn $3006.86, which is a few hundred more than the savings in interest.

However, there's a big catch to this. Extra payments to the loan pays down the loan itself; it's like making a future payment today. Extra payments to the investment does not pay down the loan--you still have to cough up the money for the loan itself. So actually, you want to earn back the total amount of the extra payments, AND exceed the savings in interest. I'd need to earn at least $6870.51 (extra payments) + $2708.12 (savings in interest) = $9578.64.

If that's the case, I'll need a rate of return of 18.13% to break even in 104 months. If I want to break even in 176 months instead, I'll only need a rate of return on 8.3%, which is much more reasonable.

However, there's another angle to consider. Any extra cash thrown at the loan will only result in a lump-sum savings in interest. Extra cash put into a mutual fund, however, will compound for as long as it is invested. And you can keep it invested for longer than 104 months, or 176 months. And the longer you keep it invested, the more you'll earn.

I think the conclusion to be drawn is that accelerating repayment is advantageous in the short-run (e.g. over the loan repayment period), especially if you pay a good chunk extra on the principal each month. But if you don't pay as much extra, or if you're thinking long term, that extra money is better off in a mutual fund.

I think I'm not going to accelerate repayment. I'm fine with delaying immediate gratification in favor of better long-term returns.

And it's much easier to justify not paying extra when you don't have the funds, anyway.

Posted in

Quantitate!

|

4 Comments »

September 9th, 2006 at 01:55 pm

In light of all the investment talk of the past few entries, I have a confession to make.

I used to be scared of investing.

Oh, I "knew" that it was the "smart/right" thing to do with your extra money. And that if you do it "well", your money can "work for you", and theoretically multiply itself into unimaginable proportions.

But I didn't trust it in my *gut*. I didn't feel comfortable or confident. What does it mean for money to "work" for you, anyway? You're the only one who can do *real* work. Earning money from the stock market seemed so... intangible. Abstract. Fake, even.

And I've never been much of a risk taker. I've always preferred to play it safe. When I *have* money, I want to *keep* it, and *know* that it's there in the bank, not in perpetually fluctuating share prices. When it earns, it's not real to me, and when it loses, I feel sick.

Interest from a bank--now that's concrete. That's real. That's dependable. And if I have to sacrifice possibly higher returns, then so be it. After all, I'm a frugal person. I can work hard, and make what I earn be enough. I'm not a spendthrift who can ever spend a million dollars, nor do I need to make that money off the stock market. I just gotta keep chugging and saving.

That was me, all of one month ago.

What made me change my mind? Simply the following train of thought.

Assuming that I start work at age 20, retire at age 65, and die at age 90, I will work for 45 years, and be retired for 25.

That means I'll be retired for 25 / (45 + 25) = 35.7% of my adult life. Thus, I'll need to save 35.7% of my salary if I want to keep cash flow and standard-of-living consistent during my working and retirement years.

That seems a bit high, but okay. I'm capable of saving that. Heck, I'm probably capable of saving more if I put my mind to it.

But hang on a second, what if I plugged in some real numbers? Say I wanted to have $40K/year income during retirement. This isn't an extravagant or unreasonable figure, especially considering inflation. Over 25 years, that adds up to...

...one million dollars.

*double-take*

Yup, it's one million all right. "I'm not a spendthrift who'll ever spend a million," eh? Well, I sure am eating my words now. But at least it's better than eating them at age 65 when I have, um, nothing else to eat.

That realization caused me to set my retirement goal at one million. And actually, that's a conservative goal, because not only am I concerned about inflation, I'm also worried about the increased medical care costs (such as prescription drugs) associated with being elderly. I may not be happy about degrading health as one ages, but I'm not in denial, either. So I'd actually like to have two million in order to feel reasonably secure.

Well, can I reach that goal? Let's see...

I'm making $32K/year. At that rate, $1.44 million will pass through my hands over the course of my entire working career.

That's not enough to put away one million, but I won't be staying at this job forever. My income will surely rise if I become a professor or go into industry. But it'll also decrease if I go to grad school, and remain the same if I do the postdoc grind.

No matter how I played with the numbers, even the most optimistic lifetime earnings projections never hit three million.

And this was assuming NO time off for children (and the costs associated with raising them!), unemployment, medical emergencies, or personal/natural disasters.

Oh, and it's also before taxes and living expenses are taken out. Since those are, you know, totally minor.

I also analyzed the situation from a different perspective.

If $40K/year is 35.7% of my annual income, my annual income must be...

...$112K.

But in that income tax bracket, I'll be losing around 45% of my income to taxes. If I'm saving 35.7% for retirement, that leaves me... 19% of my income to actually live on.

That's slightly over $20,000 per year. That's actually how much I've got now, after taxes. Buy a house on this income? I'm dreaming.

That's when it truly hit me. I *can't* save enough to properly fund retirement. It's just not feasible. If I make $2.5 million during my lifetime and take out $1 million for 25 years of retirement, I'll have $1.5 million left for 45 years of PRE-retirement. Or I'm going to have to somehow raise my annual income to something much higher than $112K/year, and do it, well, NOW.

It's just not going to work.

I *need* to invest. Without those returns, I won't make it. It's as simple as that. I know you can also use real estate, but that's a form of investment, as well--one that takes more capital than I'll have in a very long while.

So... that's why I am investing. It's risky in the same way driving motor vehicles is risky--yes, you can crash, but the vast majority of the time, you'll get where you're going. And if you do crash, chances are, you will recover and not die, especially if you've buckled up (diversified).

How far I've come in just one month. Now if only I can convince my mother that I haven't gone bat sh*t insane... She harbors my old view on investing, and she's horrified by what I'm thinking/doing. Oy.

Posted in

Quantitate!,

Musings

|

6 Comments »

August 19th, 2006 at 12:01 pm

David Bach says: "Pay yourself first," eh?

All right, then. Here's my new monthly budget plan, based on his advice. I know that he thinks that budgets don't work, but I probably wasn't the type of person he had in mind. I 'budget' all the unavoidable expenses so that I know exactly how much I can pay myself with afterwards. It's not like I need a budget to help me limit my spending.

Okay, let's start off with income.

At $16.15/hr and 37.5 hr/wk, I'm making a gross of $2600/mo. Furthermore, my gross income for 2006 will total around $17,400.

I still don't know how much taxes I'll owe, but my father is sending me last year's tax software Any Day Now. He also says that after plugging my figures, I should not owe more than $900 in taxes for 2006.

So that gives me around $2350/mo to work with. I think. I hope.

Paying others (boo):

Rent: $500 (sigh)

Utilities: no clue yet, guestimate $100 total?

I try to save by not plugging in my second and third computers, and turning off the one I do use when I'm away at work, but sometimes, I wonder why I even bother. My roommate has tons of electronics, runs the AC all day/night even when it's not hot, and wastes gas by burning his food by leaving the stove on for an hour.

Groceries: $100

Even though I don't spend more than $60 most months, I always allow myself $100, because skimping on food seems... unwise and unnecessary. And I might actually end up accidentally starving myself if I don't cut myself some slack here (I've actually lost weight... which is NOT GOOD). But I can make an effort to take the extra $40 that I never spend and put it towards paying myself at the end of the month.

Student loans: $134

That's the amount due for Stafford, starting September, which I've put on automatic debit (yeah, automation! Reduced my interest rate by 0.25%, too!). I still haven't decided if I want to accelerate repayment on this because I've been hearing mixed reports. But at least the interest is tax-deductible!

Union dues: $40

I get free health insurance and dental thanks the our union. I fully support them, and don't begrudge them their dues. I just have to turn in my member registration form!

Now, for the good stuff. Paying myself (in approximate order of importance):

Roth IRA: $333.33/mo

This will max out the $4000/year contribution limit over the course of 12 months. My father says he'll make up the rest if I don't make it to $4000 this year, but I think I can do it on my own.

I currently have $8262.09 in two Roth IRAs in Bank of America. These were deposited by my father for me a few years back when I was still young and naive and had no idea what he was doing and thought it was all quite silly to start saving for retirement so early. *whacks younger self in the face repeatedly with something smelly*

Anyway, the rates suck, so I want to roll it over to Vanguard. Except Vanguard requires a minimum balance of $5000 to waive the maintenance fee. And while one of my BoA Roth IRAs has matured (the one worth $6000, so I can satisfy Vanguard's minimum), the other one does not mature until next March. But if I move the matured Roth IRA, I'll be hit with a charge from BoA for dropping below its minimum.

Argh.

I'm still trying to figure out how to resolve this mess. This is why I haven't signed up for a Vanguard Roth IRA yet. But when I do, I will AUTOMATE the $333.33/mo transfer.

403(b): 20% (~$520 pre-tax)

In order to max out the $15,000 yearly contribution, I'd have to deduct $1250 per month. While I'd love to do max this out as well, I don't think I can handle a >50% paycheck reduction.

David Bach recommends at least 10%, which would be around $260 for me. But I think I can handle 15%, which is why I made it 20%, or $520.

Now, I just have to GET OFF MY LAZY ASS AND FILL IN THE VANGUARD FORMS AND TURN THEM IN. *cracks whip*

Car fund: $400

My car fund has a target goal of $5000 in 12 months, or about $400/mo. I may not end up spending it in a year, but it'll be good to have this around when I do finally get around to buying a car.

House fund: $40

Although a house down payment is many, many years down the line, I feel like I should start saving for it now. Can't hurt, right? The car fund gets priority for now, but once the car fund is fulfilled, that money will probably go here. And in the meantime, I think this is where I'll plop my excess grocery money.

Emergency fund: $100

If I should have at least 3 months worth of expenses in it, then $3000 is my target. I'm going to keep this conservative for now.

Savings: whatever is left

I'm terrified that I won't have anything left to go here at the end of the month, though. This is so weird for me, because I'm used to putting *all* of my unspent money into savings, which amounts to half (or more) of my paycheck. But now, I'm "paying" myself so much that I'll hardly have anything left!

And my savings will need to fund any shortages to my Roth IRA maximum, as well as any unforeseen expenses, such as clothing, public transportation fares, and dental co-pays (I'm in serious denial about the existence of cavities). And this will probably also need to supplement my various funds (car, house, emergency).

I know this should be right, but why do I feel so panicky? Am I cutting it too close? Doing too much too soon? What if I can't handle this? I do have a father-supplied savings buffer, but I don't allow myself to see it as touchable. If I end up dipping into it, then I'll have to re-evaluate this budget.

I know I still need to discuss cash flow, but I think I'll put it in a new post. This one is overwhelming enough as it is.

Posted in

Quantitate!,

Planning

|

7 Comments »

August 18th, 2006 at 05:25 am

A bit of good news, at last.

I found a bus that goes to/from New Haven to a Park & Ride Lot four miles outside of Middletown.

I'd still need a car, but this cuts costs drastically.

I decrease my daily mileage from 60 mi to 8 mi, for a decrease of 87%! Plus, I save on $100/mo parking. And I probably can get a cheaper car, since it won't be driven so hard.

The bus fare is $3.60 per way, for a total of $180/mo--if there is no commuter discount/monthly pass, which I can investigate. But with the savings in gas and parking, I still come out $100 on top, compared to the previous estimate.

And the bus schedule is perfectly synch'ed with my work day.

This just might work.

*crosses fingers*

Posted in

Quantitate!,

Planning

|

0 Comments »

August 16th, 2006 at 06:02 am

I've been thinking of buying a car.

I don't even have a driver's license yet.

Everyone thinks I'm some sort of weirdo-freak for not driving (um, grew up in New York City?) and is not sure how I get by without one (by walking, taking public transportation and carpooling?). People keep telling me that I'll need to get a car eventually, so stop resisting already. But I counter by saying that I get along fine, and I'm saving loads of money--and the environment, to boot.

Why am I finally considering it? Because I'm a sucker who misses her bf in Middletown, and he doesn't drive either. If I moved back to Middletown, I could room with him for cheaper rent, but I'd have get a car and drive to New Haven to work.

So I thought I'd crunch some numbers and get a sense.

According to my father, he says I should expect to spend $4000 to $6000 on a decent, fuel-efficient used car. I'll trust him, since he's neither trying to sell me a cheap junker that will get me killed, nor persuade me to overspend on something I don't need.

Now, I just signed a one year lease in New Haven. That means I'll have a year to save (and learn to drive!), since I'd really rather not take out a car loan.

I'd have to put away $500 per month to reach $6000 in 12 months.

This does not include:

- driving lessons (at $30/hr)

- driver's license test ($40)

- actual license ($77)

- license plate/registration ($150)

And then after I get the car, I have to continually feed it money monthly. Here are the figures, as far as I can estimate them:

- insurance: $800/year (get it with my family)

- parking: $90/month (ouch, right??!)

- gas: 60 miles/day round-trip at 30 mpg and $3/gallon for 25 days = $150/month

- maintenance: ???

- property tax: $360/year

Rounding up on the gas, since I'm sure that particular figure is tragically optimistic, everything comes out to be about $400/month.

All of this (one year of saving $500/month, plus $400/month afterwards) for the opportunity to split $775/mo rent, heat not included. (I'm currently paying $500/mo w/ heat included.) Oh, and the joy of seeing my bf every day.

Wow, the frugal part of me is screaming that it is SO NOT WORTH IT.

Then why have I put saving for the car into my budget?

Damn it. DAMN IT. *whacks oxytocin upside the head*

Posted in

Quantitate!,

Planning

|

10 Comments »

August 9th, 2006 at 02:53 am

So, the take-home verdict is in. My monthly income should be $2,025.962, but I'll be rounding that down to $2,000 for the sake of paranoia and Nice Round Numbers.

Ahead comes guestimations of future expenses.

Rent: $500

This is with a roommate. At least it includes heat and hot water, is close to the shuttle bus, and is within reasonable walking distance of my favorite grocery store.

Electricity: $20

This is split with the roommate.

Internet: $30

Also split with roommate. Can't live without broadband. This expense doubles as entertainment in the form of internet radio and bittorrent.

Natural gas: $50

Don't really know if this is accurate, but I'll probably be footing the bill for this one alone, since I am the sole cook of the household.

Groceries: $100

I budget $100, but I usually spend $60 - $80. I also get the use and abuse the CostCo membership of my roomie. Yay! Bulk nonperishables, here I come!

Student loans: $250

Again, an overestimate of what I'm required to pay, which is $133 for my Stafford, the only loan currently in repayment.

Retirement: $150

This figure is another random shot in the dark. I need to do more careful analysis before deciding on the final amount.

Savings: $900

Over a period of 12 months... that's approximately $10K into savings? If these projections hold true... Only time will tell.

Posted in

Quantitate!,

Planning

|

0 Comments »

August 8th, 2006 at 04:29 am

Here goes nothing...

Hourly income = $16.15

Weekly hours = 37.5

Weeks annually = 52

Annual income = (hourly income)*(weekly hours)*(weeks annually)

= (16.15)*(37.5)*(52)

= $31,492.5

Filing as single, and according to this IRS page,

http://www.irs.gov/formspubs/article/0,,id=150856,00.html

I'm in the $30,650 - $74,200 bracket, which means that I pay $4,220.00 plus 25% of the amount over $30,650.

So I'll owe the following in federal income taxes:

4220 + (annual income - 30650)*(.25)

= 4220 + (31492.5 - 30650)*(.25)

= $4,430.625

Now, for Medicare, at 1.45% (is this income bracket dependent?) = (annual income)*(0.0145)

= (31492.5)*(0.0145)

= $456.64

Social security, at 6.2% = (annual income)*(0.062)

= (31492.5)*(0.062)

= $1,952.535

State income taxes for CT:

http://www.ct.gov/drs/cwp/view.asp?A=1510&Q=308248

http://www.ct.gov/drs/lib/drs/forms/2006forms/income/ct-1040es.pdf

Um... *does twenty calculations and shakes the magic eight ball...*

$341.156??

Yeah, I won't be counting on that figure too much. I had to skip a few steps that I didn't understand, hence the lack of documentation on here. That was way too complicated.

Total taxes = (federal income tax) + (medicaid) + (social security) + (CT income tax)

= 4,430.625 + 456.64 + 1,952.535 + 341.156

= $7,180.956

Take-home income = (annual income) - (total taxes)

= 31,492.5 - 7,180.956

= $24,311.544

Erm, yeah. I'll be so impressed if that figure is anywhere close to accurate.

D'oh, I think I have a headache now. Not to mention fully traumatized. But I finished item 1 in my to-do list.

Posted in

Quantitate!

|

7 Comments »

|