April 13th, 2015 at 01:33 am

Posted in

Quantitate!

|

2 Comments »

April 10th, 2015 at 08:51 am

Quick snapshot of the financial situation as of close of business 9-Apr-15:

Cash: $16,297.63

Home: $169,378 minus ($129,766.66) mortgage = $39,611.34 equity

Car: $13,900

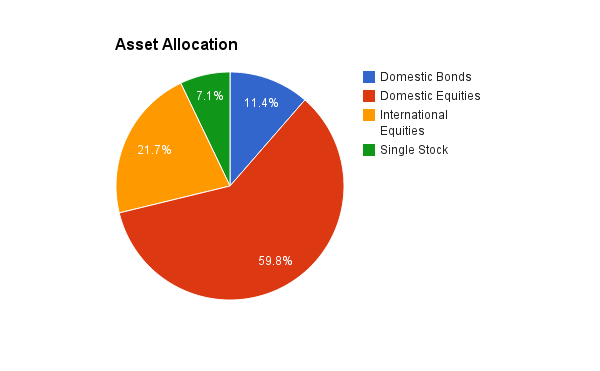

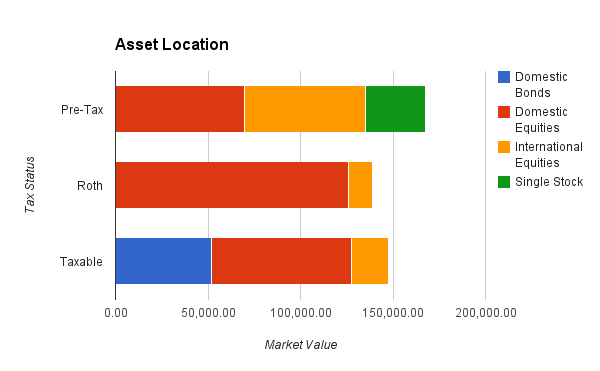

Investments: $749,901.40

- 401(k): $113,746.98

- Roth IRA: $115,696.03

- Rollover IRA: $65,449.31

- Rollover IRA Brokerage: $9818.84

- HSA: $1132.78 (currently in cash; need $2500 minimum balance to invest)

- Taxable: $149,983.61

- Stock Options: $294,073.85 vested (out of $504,931.90 total)

Net Worth: $819,710.37

In recent weeks/months, I've made the following adjustments to my portfolio:

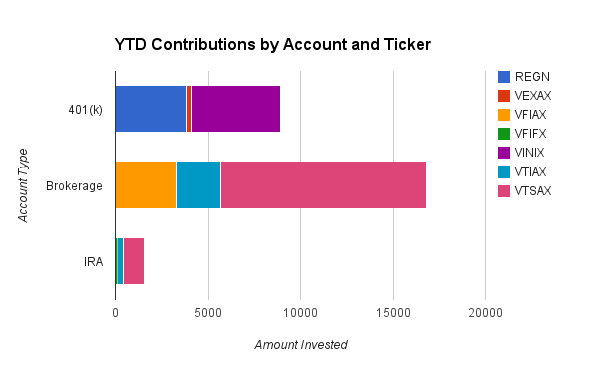

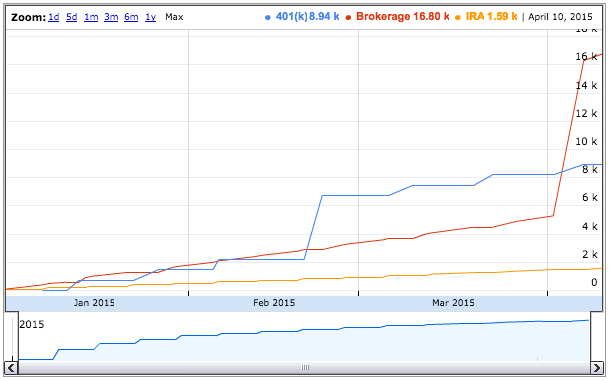

- Swapped 20% of my 401(k) from Vanguard Institutional Index (VINIX) to Vanguard Extended Market Index (VEXAX) to approximate the Vanguard Total Stock Market Index (VTSAX, which I can't get directly in my 401(k)), and balanced my future contributions to be an 80/20 split.

- Seeded $11K from money market into a taxable VTSAX holding, and will henceforth be using that instead of my S&P500 holding, which I'm retiring.

- Increased my taxable investments from $400/week to $500/week -- because I got a raise and bonus at the end of last year, and what else am I gonna do with it? :P

- Killed my (brand-new  ) traditional IRA. I apparently make too much money to take the deduction now.

) traditional IRA. I apparently make too much money to take the deduction now.

- I want my domestic to international equities ratio to be 2:1, but I'm at 2.76:1 right now, so I'm aggressively rebalancing my AA more towards international without triggering taxes. All of my Roth IRA and 80% of my taxable contributions are going towards Vanguard Total International (VTIAX). If this approach is taking too long (e.g. if by next quarter that ratio has barely shifted), I might buy/sell within my Roth space, or rebalance my 401(k) contributions.

I set a goal in Mint where I called reaching $1M in assets (excluding home/car equity and HSA) "FIRE", and the projected completion date is sometime in 2017 (April 27 at the moment, but it jumps around a lot). I love the fact that market appreciation is actually dwarfing my (fairly substantial) monthly contributions. Go Go Gadget Compound Interest!

Posted in

Quantitate!,

Early Retirement,

Investing

|

2 Comments »